2023 insolvency statistics – annual review

ServicesFinancial advisoryRestructuring and insolvency servicesRestructuring & Insolvency InsightsMonthly insolvency statistics

2023 insolvency statistics – annual review

A review of corporate and personal insolvencies across the UK in 2023.

Corporate Insolvencies

England and Wales

Company insolvencies in 2023 totalled 25,159 which was both a 14% increase on 2022 and a 46% increase on 2019. These increases could be seen as evidence of the combined pressures of Brexit, Covid-19 and inflation (to name but a few) having taken effect in the last 12 months with many of the companies that were supported during the pandemic now being unable to recover. Given the economic pressures, it is likely that it may be many months before we start to see a decline in companies entering insolvency.

The increase in total company insolvencies has been primarily driven by the high number of companies entering a Creditors’ Voluntary Liquidation (CVL). There were 20,579 new CVLs in 2023 which was a 9% increase on 2022 and a 71% increase on 2019.

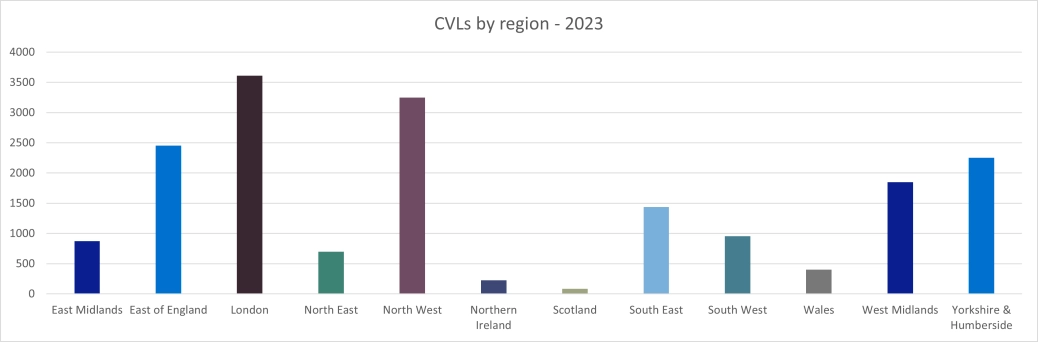

In 2019, 39% of all CVLs were administered by their Liquidators in London and 23% in the North West. However, in 2023, whilst there remained high volumes in the afore-mentioned regions, there was a more even spread across the country with increased volumes across all the regions, and in particular, the East of England.

Hospitality was one of the primary business sectors most affected by the pandemic, with a large number of businesses taking out loans to survive. Many companies within that sector have faced significant financial strain due to increases in energy costs, interest rates and inflation on food and drink leading to the highest number of CVLs by sector in 2023. Whilst the UK Government has committed in its 2023 Autumn Statement to extending the relief available in this sector, it remains to be seen whether this additional support will be enough to stem the rise in failures in the sector.

The pandemic created a significant backlog of winding up petitions which are now in the process of being addressed, 2023 saw an increase in compulsory liquidations of 44% compared to 2022 and a return to a similar position as 2019. The numbers in 2024 could be expected to rise slightly but may be tempered by policy decision and court backlogs.

Whilst there was a decrease in December 2023 this is consistent with trend in previous years.

After the historical lows seen during the pandemic due to the protective measures implemented by the government, HM Revenue & Customs has become increasingly aggressive this year with regards to issuing winding up petitions. The number of winding up petitions issued by HM Revenue & Customs increased by nearly 3.5 times compared to 2022, indicating a toughening in policy towards those companies defaulting on paying their taxes. The top 5 petitioning creditors are shown below – please contact us should you require any further information.

The number of administrations increased by 27% to 1,527 when compared to 2023 but reduced by 14% when compared to 2019. The increasing liquidation procedures and falling administrations is interesting as it indicates a deterioration in the more positive outcomes of insolvency, with fewer jobs and businesses being saved and more businesses simply closing their doors.

On closer inspection and following the recent press coverage regarding the construction sector, it will be unsurprising that it was the leading sector for Administrations in 2023. This sector is particularly vulnerable to financial distress which is in part due to the nature of contract cycles, leading to poor cash flow management. The main challenges facing this sector include labour shortages, slowing project volumes, inflationary effect on raw materials, on-going supply challenges with an increase in regulation and new environmental standards. The above can be particularly damaging when contracts are based on a fixed price and can be agreed a number of years ahead of the works being undertaken and completed.

Other notable sectors in 2023 include Real Estate (interest rate rises), Haulage (rising fuel costs, driver shortages and environmental pressure) and Hospitality (labour shortages) highlighted earlier.

The insolvency figures for 2023 saw a 68% increase in CVA numbers to 186 when compared to 2022. However, there was a 48% reduction in numbers when compared to 2019. Along with the rise in liquidations and an increase in debt levels, it would indicate over the longer term that less companies are currently able to come to an arrangement with their creditors quite possibly due to the significant uncertainties around future trading.

Scotland

In 2023 there were 1,234 company insolvencies registered in Scotland, 16% higher than 2022 and 20% higher than in 2019. With reference to our previous updates, this increase is driven by a rise in CVLs.

Northern Ireland

In 2023 there were 215 company insolvencies registered in Northern Ireland, 38% lower than 2019 and on a similar level to 2022. This decrease from 2019 levels is due to a significant reduction in the number of compulsory liquidations.

Personal Insolvency Statistics – 2023

Headlines – England and Wales

Personal Insolvency numbers for 2023 decreased from 2022 with a monthly average of 8,621 people entering a formal insolvency procedure, compared to an average of 9,897 in the previous year.

The reduction was driven by a marked drop in the number proposing an Individual Voluntary Arrangement (IVA), down from the record numbers in 2022.

The number of bankruptcies has steadily increased from 2022 levels, following a marked downward trend during the pandemic.

Debt Relief Orders (DRO’s) have shown a marked increase on the previous year’s monthly average, recovering to pre-pandemic levels.

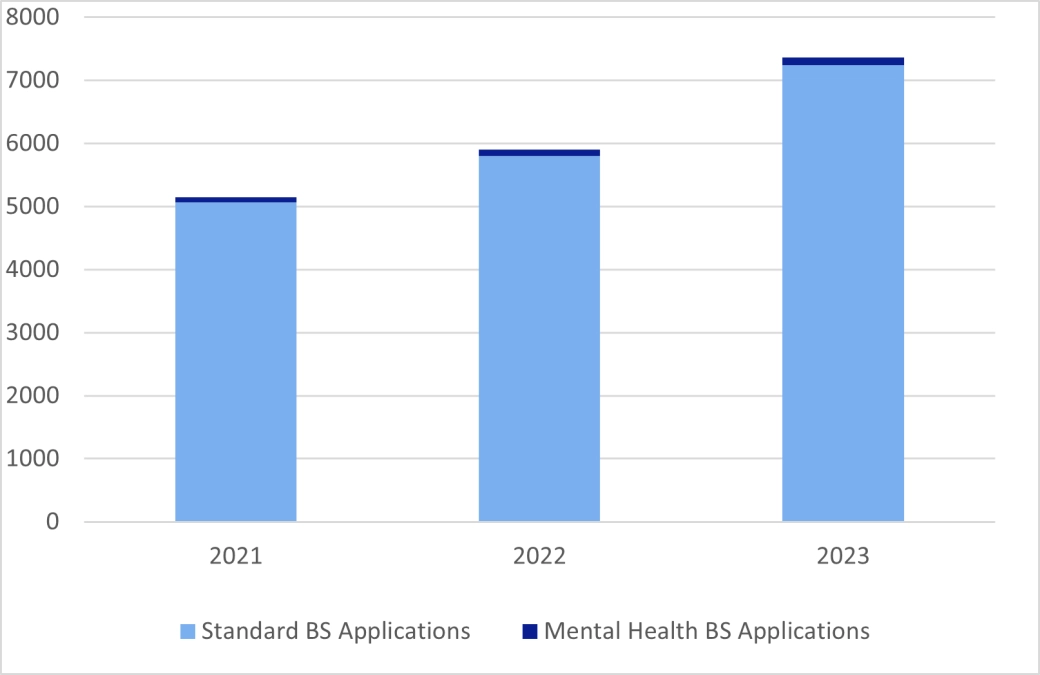

Breathing Space (BS) applications have increased year on year since inception, with an average of 7,366 in 2023, up from 5,898 in 2022.

Standard BS applications had averaged 7,244 per month in 2023, compared to 5,796 in 2022, whilst Mental Health BS applications have also increased, with an average of 122 in 2023, up from 101 last year.

What’s behind the numbers?

IVA’s have shown a marked decrease in 2023, from historical highs in 2022. There was a monthly average of 5,338 IVA’s in 2023, down from 7,322 in 2022. This is a result of the Financial Conduct Authority clamping down on debt packaging firms; the Insolvency Service issuing guidance to Insolvency Practitioners (IPs) on their marketing techniques; ensuring stricter criteria, more robust compliance processes, and tougher sanctions on individual IP’s.

Following the changes in criteria from May 2021, allowing easier entry into a DRO, numbers have increased quite markedly with a monthly average of 2,643 in 2023, compared to 2,018 in 2022.

A “new” DRO would have previously been a bankruptcy, and therefore, the bankruptcy numbers decreasing is no real surprise. In 2023, there were 7,677 bankruptcies, a monthly average of 640. In 2022, there were 6,680 bankruptcies, with a monthly average of 557, showing a slight increase in numbers, however, still significantly lower than pre-covid levels.

Bankruptcy petitions are being increasingly filed, especially by HMRC in pursuit of unpaid tax, and creditors’ petitions have increased, with a monthly average of 140 in 2023, compared to 95 in 2022. However, when compared to 2019’s average of 261 petitions per month, there is still some way to go to reach those levels again.

Debtors’ applications for bankruptcy have increased, with a monthly average of 500 in 2023, compared to 462 in 2022. Again, these numbers are still significantly down on the pre-covid levels of 902 in 2020 and 1,135 in 2019.

The spike in BS applications is driven largely by public awareness but more significantly by appropriate signposting by the debt advisory sector.

Demographic Profile

|

|

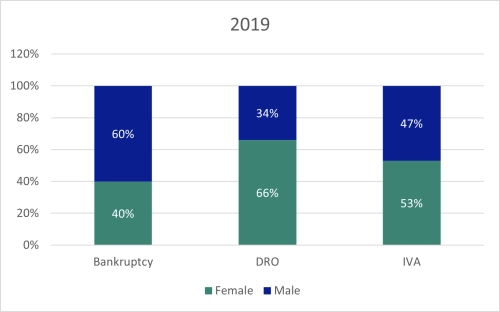

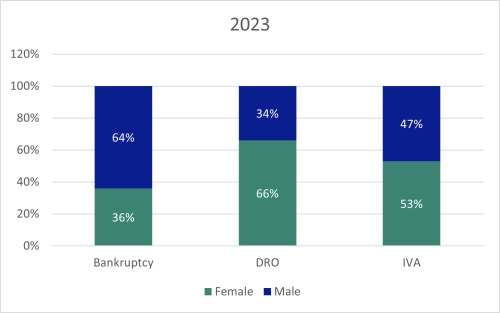

In 2023, the gender profile for individuals entering into formal insolvency solutions has remained relatively static since 2019. However, it is interesting to note that an increased proportion of men (4%) became bankrupt. This shift towards a greater percentage of males entering bankruptcy may well stem from the impact that the pandemic had on self-employed businesses such as construction contractors.

|

|

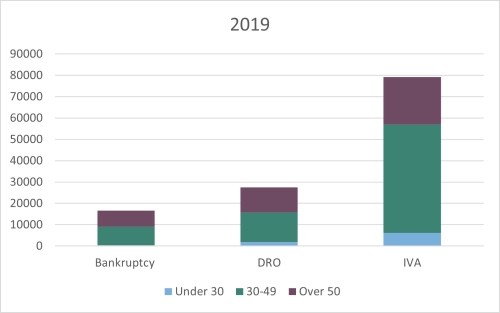

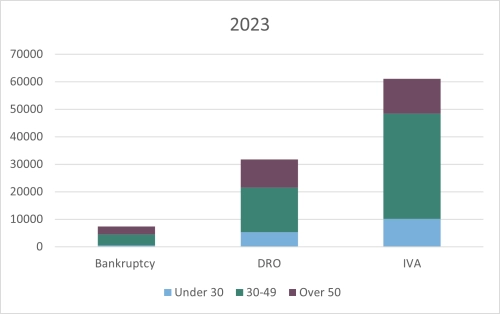

Bankruptcy remains the chosen option for those above 30 years old and the split between those either side of 50 is also fairly constant.

Between 2019 and 2023 there appears to be a marked increase in the percentage of under 30’s using DRO’s as their chosen option. During the same period the percentage of under-50’s choosing DRO’s has increased significantly. This has largely been driven by the entry criteria making it easier for younger people to deal with their indebtedness.

IVA’s seem to have grown less popular with the over-50’s, and more popular with the under 30’s. This has largely been driven by regulatory pressure leading to better advice and more appropriate solutions.

Predictions for 2024

The increase in BS applications may well continue into 2024, however, this procedure, as the name suggests, is merely a pause in the process and the individuals concerned will still have to deal with their indebtedness. What course of action they take will remain to be seen. It is hoped that some statistics on post-BS outcomes will be made available in 2024 to properly monitor the success of the legislation. Please see here for more information.

The IVA market now seems to have found a level, and it is hoped that appropriate advice will lead to positive outcomes for both debtor and creditor. Rather than there being 7,000 IVA’s per month, with a large percentage of those failing, it is better to see a smaller number of quality IVA’s staying the distance. Those avoiding inappropriate IVA’s will need an alternative solution and it is hoped that they find the best path via quality advice.

DRO’s may level out during 2024 and find their plateau of around 2,750 per month. However, if those referred to above, who escaped entering a badly advised IVA choose a DRO as their ‘plan B’, then we could well see the DRO numbers swell. Equally, those exiting BS may also adopt the DRO route as their chosen option.

Creditor petitions should continue their upward trend into 2024 and beyond. If HMRC are seen as the benchmark for other government departments (e.g. Councils), then petition numbers could be significant. Other creditors may well see HMRC’s conduct as a green light to petition themselves, having shown great forbearance during the pandemic. Again, those avoiding IVA’s, or coming out of BS, may well also choose an application for bankruptcy as their option, especially where the DRO criteria is out of their reach.

Current Personal Insolvency procedures received mixed views during a recent government consultation. Modernising the current framework could result in a single gateway to enable people to access independent, regulated debt advice, via a digital platform, or dovetailed with the current BS scheme.

The summary of responses leans towards the need for some reform, with new proposals expected to be forthcoming in 2024.

Ed Thomas, Director in Personal Insolvency operations, commented:

“The consultation was important and timely, with a significant percentage of the population facing financial pressures. Mental health and vulnerability issues require the removal of barriers into appropriate and regulated insolvency procedures, providing a way out of debt. The new framework must provide equally good outcomes for creditors where possible.”

Northern Ireland

Individual insolvencies in 2023 remained lower than pre-pandemic levels with 43% and 12% decreases compared to 2019 and 2022 respectively.

National contacts

Michael Pallott Partner - Restructuring and Insolvency - London

Paul Rouse Partner – Head of Restructuring and Insolvency - London