We support banks in addressing climate risk in their risk management frameworks, from setting the right governance, coming up with a climate-resilient strategy, enforcing their risk management, and reporting on climate risk.

Our solutions provide support to banks in climate risk evaluation, climate stress testing and scenario analysis.

Climate change is recognised as a serious threat to financial institutions and the stability of the global financial system. Unfolding physical risks together with increasing regulatory expectations pose challenges to how banks management their risk exposure. To respond to these developments, banks will have to build their capabilities in identifying, quantifying, and disclosing their exposure to climate risks and incorporate climate change consideration within their traditional financial risk management.

Our resources to support you with climate risk and risk management frameworks:

Climate risk encompasses the potential financial and operational impacts arising from climate change, including both physical risks (e.g., extreme weather events) and transition risks (e.g., policy changes, market shifts).

Physical risk involves the direct impact of climate change on assets, infrastructure and operations, such as damage from extreme weather events, rising sea levels and long-term shifts in climate patterns. Physical risks are divided into two categories:

Acute risks relate to extreme, abnormal climate and weather events such as floods, heat stress, wildfires and hurricanes.

Chronic risks relate to long-term changes to the environment and weather patterns. They arise from progressive shifts, such as increasing temperatures, sea-level rises, water stress, biodiversity loss, land use change, resource scarcity or habitat destruction.

Transition risks arise from the implementation of new policies and regulations aimed at achieving net-zero emissions and a more sustainable economy, which entails significant structural changes to the economy. These transition risks could be triggered by:

Changes in regulations and policies such as increased pricing of greenhouse gas (GHG) emissions due to carbon taxation, direct regulation, enhanced emissions reporting, etc.

Changes in technology such as renewable energy, carbon capture and storage, lower emissions technology, etc.

Changes in consumer preferencesand investment strategies, including changes in demand for carbon-intensive transport, energy-efficient housing and appliances, reputational risks, etc.

Change in reputation caused by increased stakeholder concern regarding the impact of companies on the environment or the stigmatisation of certain sectors.

How are banks impacted by climate risk?

Banks are affected by climate risk through potential credit losses, market volatility, operational disruptions and increased regulatory scrutiny. These risks can impact their financial stability and long-term viability.The Bank of International Settlements (BIS) defines climate-related financial risks as “the potential risks that may arise from climate change or from efforts to mitigate climate change, their related impacts and their economic and financial consequences”.

What regulations apply to climate risk in the UK, EU and North America?

In Europe, both the European Central Bank (ECB) and the European Banking Authority (EBA) have established frameworks to manage climate-related risks for financial institutions. The ECB published its Guide on climate-related and environmental risks in November 2020 and the EBA published the consultation paper, Guidelines on the management of ESG risks, in January 2024 to explore how these risks can be incorporated into the prudential framework.

In Canada, the Office of the Superintendent of Financial Institutions (OSFI) has issued a Climate Risk Management guideline outlining expectations for governance, risk management and climate-related financial disclosures. It includes requirements for climate scenario analysis, stress testing and capital and liquidity adequacy.

What are the key elements of climate risk assessment?

Climate risk assessment involves analysing exposure to physical and transition risks, evaluating potential financial impacts and integrating climate risk into overall risk management strategies. The main steps are as follows:

Risk Identification: Understand and identify the types of climate risks faced by the organization and assess its vulnerability to them.

Risk Assessment: Institutions utilise scenario analysis to evaluate the potential financial impacts of various climate scenarios. This process helps firms understand how different climate-related risks could affect asset values, liabilities and overall financial stability. It is essential to define models that translate climate risks into financial risks by considering their potentiality, vulnerability and impacts.

Integration into Financial Risk Management: Climate risks are incorporated into existing risk management processes, including capital allocation, loan approvals and portfolio monitoring. Consequently, climate risk can be seen as a risk in itself or as a driver for more traditional financial risks (credit, market, etc.).

What are the main climate scenarios?

Main climate scenarios include various projections of future climate conditions based on different levels of GHG emissions, such as the Representative Concentration Pathways (RCPs) and Shared Socioeconomic Pathways (SSPs). Climate scenarios are usually long-term scenarios based on extensive analysis and modelling of key factors such as demography, energy demand projections, emission pathways, carbon budgets and policy and technology assumptions. Regulators and independent companies are also developing their own scenarios:

The objective of climate stress testing is to assess the resilience of financial institutions when faced with climate-related risks by simulating various adverse climate scenarios and evaluating their potential impacts in the short medium and long term.

What are the climate-related reporting standards?

Climate-related reporting standards are frameworks and guidelines that help organizations disclose information about their climate-related risks, opportunities and impacts. The main reporting standards are the following:

Task Force on Climate-related Financial Disclosures (TCFD): Established by the G20’s Financial Stability Board, the TCFD provides recommendations for companies to disclose information on governance, strategy, risk management and metrics and targets related to climate change.

IFRS Sustainability Disclosure Standards: Developed by the International Sustainability Standards Board (ISSB), these include:

IFRS S1: General Requirements for Disclosure of Sustainability-related Financial Information.

IFRS S2: Climate-related Disclosures.

The Global Reporting Initiative (GRI): Provides a comprehensive set of standards for sustainability reporting, including climate-related disclosures.

The European Sustainability Reporting Standards (ESRS): A set of standards developed by the European Financial Reporting Advisory Group (EFRAG) to guide companies in disclosing their sustainability-related information.

What is the BoE’s approach to scenario analysis?

In April 2024, the BoE published an article with useful insights for financial institutions on using scenario analysis to measure climate-related financial risks. The article focuses on climate as a financial risk from a system-wide risk perspective and with regards to the BoE’s own financial operations. While not a supervisory guidance, the article explores how central banks and financial institutions can use scenario analysis to quantify these risks. It is therefore advisable for regulated firms to understand the key messages of this article and assess where they can incorporate these in their own thinking around quantifying climate risks as a part of their stress testing and ongoing operations. Find out more.

What does the Supervisory Statement 3/19 cover in the UK?

Governance Arrangements: Firms must embed the consideration of financial risks from climate change into their governance frameworks. This includes board-level oversight and clear allocation of responsibilities.

Risk Management: Banks are expected to incorporate climate-related financial risks into their existing risk management practices. This involves identifying, assessing and managing these risks as part of their overall risk management framework.

Scenario Analysis and Stress Testing: Firms should use scenario analysis to understand the potential impact of climate-related risks on their business. This helps in strategic planning and risk assessment.

Disclosure: Banks are required to develop and implement an approach to disclose their exposure to climate-related financial risks. This includes transparency in how banks manage these risks and the impact on their financial position.

External scrutiny, corporate values and financial impact are driving banks to address new challenges across business functions

CEO and Board: strategy and governance

Ensure board can provide oversight of climate related risk and opportunity.

Define and implement business strategy that considers actual/potential impact of climate risk and business opportunity.

CRO: risk identification, regulatory stress test and capital

Risk identification relating to climate risk.

Quantify impact of climate risk on asset portfolios & economic/regulatory capital.

Perform stress tests.

Monitor climate-related risk to business solvency and capital.

Implement risk mitigation for climate risk.

CFO: regulatory and financial reporting

Ensure regulatory and financial reporting includes impact on climate risk.

Produce and monitor business plan aligned with business strategy that reflects impact from climate risk.

CIO: asset allocation and security selection

Design sustainable and green investment strategy that meets business objectives.

Set top-down and bottom-up climate metrics.

Ensure they can report climate risk on investment portfolios by incorporating climate data into asset allocation and investment selection.

We provide a holistic climate risk management service offering covering:

Governance

Capability building around climate risk at the Board and Senior Management level.

Development and review of Climate-Related & Environmental (CR&E) risk management framework.

Development of appropriate key risk indicators and limits for CR&E risks.

Ensure regulatory compliance against climate risk management expectations through gap analysis and roadmap preparation.

Strategy

Transition plan design.

Climate risk appetite set up.

CR&E factor integration into business decision making.

Strategy and business planning.

Risk management:

Scenario analysis and design.

Stress testing.

Importance of granular data.

Metrics and targets:

Statistical modelling for transition and physical risk integration into credit, market and liquidity risks.

Case study: CliMate

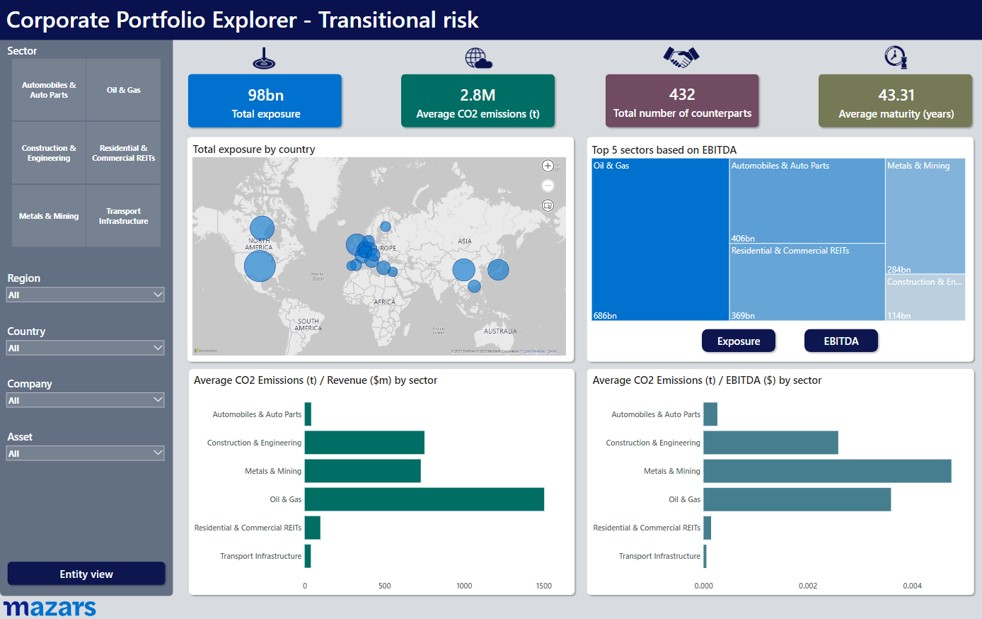

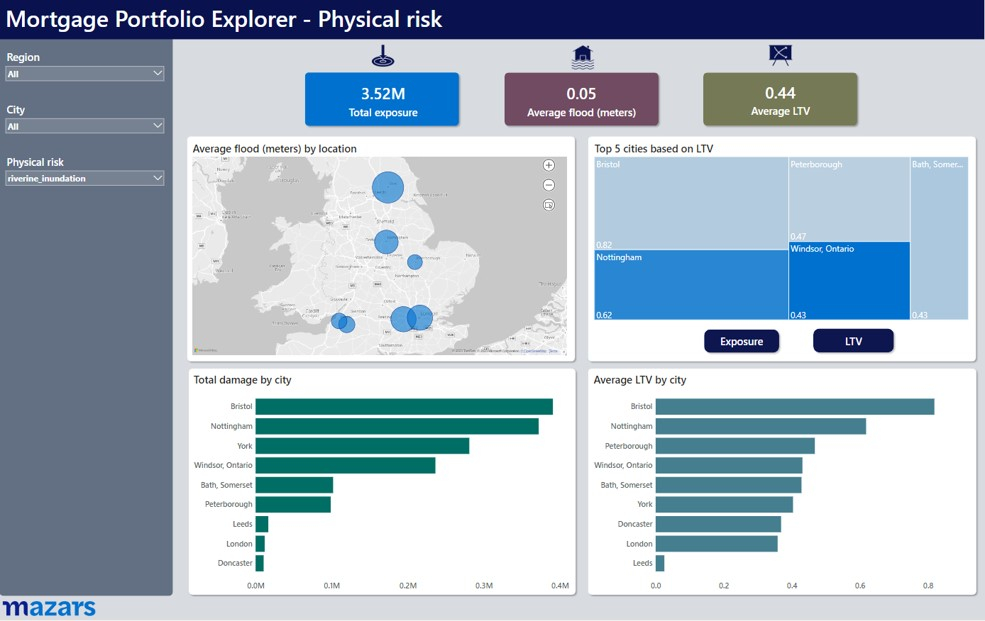

Introducing our in-house Climate Risk Assessment Tool CliMate, a solution designed to empower banks in navigating the complex landscape of climate risk. This tool is crafted to evaluate the impact of both transition and physical risks on credit risk, leveraging data from banks’ portfolios:

Portfolio Explorer: this module supports risk identification and assessment by providing key climate performance indicators. It quantifies the carbon footprint of banks’ portfolios, offering insights into their contribution to climate change. It also measures exposure to high-risk sectors such as fossil fuels and high-risk locations, enabling banks to understand the potential physical risks affecting specific assets.

Scenario Explorer: this feature allows banks to dive into various transition scenarios used for climate risk stress testing. The adaptability of CliMate ensures it can cater to a wide range of scenarios, providing flexibility to best fit the needs and requirements of each bank.

Results Explorer: this functionality enables banks to view the stress test outputs on credit risk, including expected credit loss calculations for transition risk on corporate portfolios and physical flood risk assessments for mortgage portfolios.

Supervisory Statement SS3/19 sets out expectations for how UK (re)insurance firms, banks, building societies, and PRA-designated investment firms should manage and disclose financial risks related to climate change.

In November 2024, the NGFS (Network for Greening the Financial System) [1] published phase V of its widely used climate scenarios updated with the most recent economic and climate data, policy commitments, and model versions. This phase V also introduces a new damage function for physical risk assessment.

On 17 April 2024, the Bank of England (BoE) published an article with useful insights for financial institutions on using scenario analysis to measure climate-related financial risks.

On 16 October 2023, the Office of the Superintendent of Financial Institutions (OSFI) launched a consultation on its draft methodology for the Standardized Climate Scenario Exercise (“SCSE”).

On 11 January 2024, the Prudential Risk Authority (PRA) published its Dear CEO letters addressed to insurance companies, international banks and domestic deposit takers, outlining the PRA priorities for 2024 for the respective addressees and assessing the current state of various risks including a specific focus on climate risk in the context of financial risks.

The Transitional Plan Taskforce (TPT) was formed in April 2022 to help companies from 40 sectors, including financial institutions, build and disclose their climate transition plans.