Climate-related disclosures for insurers

Climate-related disclosures have moved from voluntary to mandatory and the bar for both minimum and best practice is rising.

Our two-article series on climate-related disclosures aims to answer two questions:

The first question was tackled in our previous article Climate-related disclosures for insurers - what do they entail?. The following focuses on what steps can be taken to improve disclosures.

Regulatory requirements are different depending on the type and size of an insurer, but there are certain overarching principles that insurers need to adhere to when preparing climate-related disclosures in the financial statements. These are outlined in the previous article and include how to build disclosures around the main framework of governance, strategy, risk management and metrics and targets. These four ‘pillars’ feature in all climate disclosure requirements to some extent so building reports around them is a good place to start.

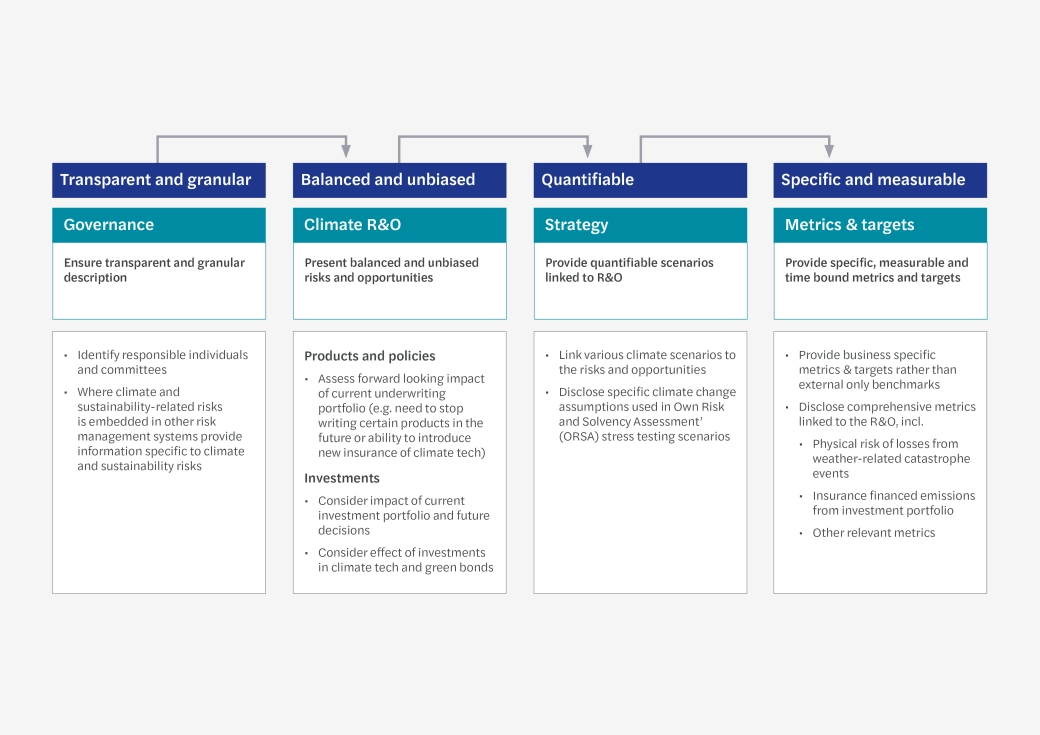

The FRC thematic review FRC TCFD disclosures and climate in the financial statements July 2022 provides recommendations on how to improve the quality of TCFD [1] disclosures. We have taken the examples of good quality disclosures and aggregated them into four key principles that can help insurers improve their climate-related reporting. The first two principles could be applicable to any insurer that is required to disclose the impact of climate risk, the rest is more relevant to larger insurers that prepare TCFD or TCFD aligned climate-related disclosures.

| Key characteristics of good quality climate-related disclosure | Relevant to: |

|---|---|

Transparent clear and granular Include clear, concise, and easily understandable information. Aligning climate disclosures with narrative and financial reporting. Avoid high level, generic information about climate change which lacks specificity considering the potential impact on the company's industry, operations, and geographical locations. Ensure disclosed information is relevant, granular and specific. | All insurers |

Balanced and Unbiased Provide balanced and unbiased disclosures regarding risks and opportunities and fair presentation of positives and negatives. Additionally these should align with the strategy of the business by identifying and quantifying the impacts of the risks and opportunities. | All insurers |

Quantifiable Assess the rigor and depth of scenario analysis. Make sure the scenario analysis includes quantifiable information and describes the methodology used. Evaluate how the board integrates climate-related considerations into the overall business strategy. | Insurers that provide TCFD and TCFD aligned climate-related disclosures |

Specific and Measurable Look for specific, measurable, and time-bound metrics and targets. Consider historical data and movement metrics to assess progress against targets. Ensure Scope 3 data is included where required and look to develop an approach to further Scope 3 emissions measuremnt. | Insurers that provide TCFD and TCFD aligned climate-related disclosures |

In addition to the above, best practice reporting should include a clear narrative thread. A coherent climate strategy underpins a consistent narrative and illustrating management commitment should also be fundamental to the report. Climate disclosures should also be aligned to principal risk disclosures.

Better quality disclosures come with a number of challenges for insurers. Firstly, it will require a significant investment of resources. There is also a commercial sensitivity challenge, nonetheless, it is important to remember eventually all market participants will be disclosing complete and accurate information, for example, Scope 3 emissions. A further challenge is the potential restatement of comparative climate-related information and the negative connotation of the word ‘restatement’. However, restatements (for example, as a result of new data obtained) demonstrate to the market that management is working towards better quality climate-related disclosures. Investor education and board members training can help to change the attitude in relation to restatements and promote better quality climate-related disclosures.

Below we provide a practical guide of how to achieve better quality disclosures regarding climate-related risks and opportunities and their governance. This information could be considered by any insurer that is required to disclose the impact of climate risk. This guide also includes further steps on strategy and metrics and targets that should be considered by the insurers that provide TCFD or TCFD aligned climate-related disclosures (including climate-related disclosures prepared in accordance with IFRS S2 in the future [2]).

While climate-related regulation is being advanced potentially regulators will further develop insurance-industry specific standards. Currently, the only accepted Insurance Sustainability accounting standard is by the SASB [3]. It is referred to internationally by the ISSB [2] as well as in the CSRD [4] regulations. The standard maps sustainability factors that are material to the insurance sector. Below we provide a condensed summary of the insurance SASB standard bringing together the examples of risks and opportunities and some related metrics suggested in the guidance:

| Topic in SASB insurance standard | Associated risks (and opportunities) for insurers | Associated metrics and targets |

|---|---|---|

| Transparent Information & Fair Advice for Customers | Failure to inform customers about products in a clear and transparent manner may result in increased consumer complaints, regulatory fines, reputation damage and adverse financial outcome. | Monetary Losses, from non-compliance. (Quantitative) Complaints-to-claims ratio. (Quantitative) Customer retention rate. (Quantitative) |

Incorporation of Environmental, Social and Governance Factors in Investment Management

| Failure to address environmental, social and governance (ESG) issues may reduce returns and limit claims settlement ability. | Description of approach to incorporation of ESG factors in investment management processes and strategies. (Discussion and analysis) |

| Policies Designed to Incentivise Responsible Behaviour | Low carbon technology, renewable energy and the development of new policy products allow insurers to limit claim payments while encouraging responsible behaviour. | Net premiums written related to energy efficiency and low carbon technology. (Quantitative) Products that promote environmentally responsible behaviours. (Discussion and analysis) |

Financed Emissions | Counterparties with higher greenhouse gas emissions might increase the level of credit, market and reputational risks of insurers. | Absolute gross financed emissions, disaggregated by Scope 1, (Quantitative) Gross exposure for each industry by asset class. (Quantitative) (Quantitative) |

| Physical Risk Exposure | Failure to assess environmental risks when underwriting insurance may result in higher-than-expected claims payments. | Probable Maximum Loss of insured products from weather-related natural catastrophes.

|

| Systemic Risk Management | Failure to comply with regulatory requirements could lead to substantial penalties. Insurers that write annuities, financial guarantees and also non-insurance related products are most likely to contribute to systematic risk being designated as Systemically Important Financial Institutions. | Total fair value of securities lending collateral assets.

Exposure to derivative instruments by category: (1) total exposure to noncentrally cleared derivatives, (2) total fair value of acceptable collateral posted with a central clearinghouse, and (3) total

Approach to managing capital- and liquidity-related risks associated with systemic non-insurance activities.

|

It is important to apply the characteristics above with proportionality and materiality in mind. The challenge of having unified characteristics for all the insurers is that the depth of disclosure varies according to the organisation’s climate change risk.

To speak to our experts about climate-related disclosures, get in touch using the button below.

Climate-related disclosures have moved from voluntary to mandatory and the bar for both minimum and best practice is rising.

Read our latest insurance insights.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.