Basel 3.1 - Bitesize

In this series of short bitesize articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

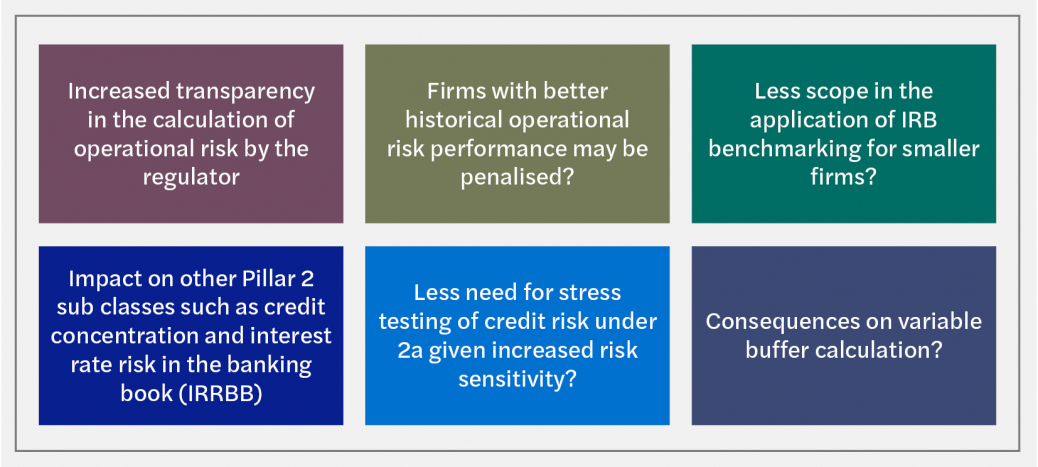

The capital framework is viewed by regulatory authorities holistically. Materially the underlying risk exposure of firms will not have changed on either side of Basel 3.1 implementation. Therefore, the overall balance of risk and capital should largely remain the same.

A good example of this can be found in operational risk. Increased requirements in Pillar 1, stemming from the beefed-up standardised approach, are likely to reduce firms Pillar 2. However, given the limited risk sensitivity stemming from neutralising the ILM, it appears that requirements in Pillar will remain material. This may cause frustration at some firms given the fact that the PRA’s Pillar 2 operational risk calculation remains something of a black box with quantitative guidance remaining very sparse. Another area which may change is credit risk. For firms on the standardised approach, there is an open question about whether the increased risk sensitivity of the Basel 3.1 proposals will reduce the need for material Pillar 2 assessments. This may include benchmarking and stress testing analysis. On the flip side, there are some risk stripes that are often linked to calculations based on nominal (for example, non-risk weight dependent) requirements. This includes interest rate risk in the banking book, although current circumstances around the failure of Silicon Valley Bank and the near demise of Credit Suisse may encourage regulators to revisit this risk type more generally. Finally, the Bank of England’s own, excellent, blog site – Bank Underground – has been openly suggesting that the current calculation of credit concentration risk is inadequate in the calculation of sectoral or geographic add-ons, for smaller firms in particular. Again, given concentration risk is once again front and centre after the collapse of Silicon Valley Bank, this element of Pillar 2 seems ripe for significant overhaul by the regulatory authorities. For Strong and Simple firms all of this could be moot. These firms can enter the Transitional Capital Regime, with requirements that are substantively the same as the existing Pillar 1 and 2 frameworks in the CRR, until the implementation date for a permanent risk-based capital regime for the simpler regime. The PRA is expected to provide much more detailed guidance around the capital regime for the Strong and Simple framework in 2024. |

What banks should consider: • The PRA is essentially looking to implement the Strong and Simple regime in tandem with the Basel 3.1 reforms. Therefore, smaller firms that may be potentially eligible for both, need to give themselves enough time and resources to run suitable cost/benefit analysis to understand which regime may suit them best. • Given that the risk sensitivity of the new standardised approach is being neutralised by the PRA, firms should expect that their Pillar 2 operational risk calculation will continue to be material, from both a qualitative and quantitative perspective, and plan accordingly. • Firms should be aware that the Pillar 2 review may cover risk stripes not directly addressed by the Basel 3.1 implementation, including IRRBB and credit concentration risk. |

If you have any further questions regarding Basel 3.1, please contact us via the button below and a member of our team will be in touch.

In this series of short bitesize articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

Under Basel 3.1, the Prudential Regulation Authority has proposed to implement changes to how firms measure market risk. These include an amended version of the preexisting simplified standardised approach (SSA) and two new calculation methodologies – an advanced standardised approach (ASA), and a new internal model approach (IMA).

The PRA has confirmed the removal of the CRR SME Supporting factor under the Standardised and IRB approaches their near final rules for Credit Risk. However, an ‘SME Lending Adjustment’ will be introduced to offset the impact on the cost of SME lending. This is with the intention of ensuring that the cost of capital for SME exposures will be net neutral under the Basel 3.1 regime.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.