Valuations - IFRS 16

Since its introduction in 2019, IFRS 16 (Leases) has become a key consideration for business valuers, our team explores its effect on various valuation metrics such as key financial metrics, enterprise value and net debt and industry multiples.

Having come into effect in January 2019, IFRS 16 has had a substantial impact on Valuations. IFRS 16 requires lessees to recognise assets and liabilities arising from almost all leases, making the distinction between ‘a lease’ and ‘a service’ essential. This standard affects the valuations of companies who report under IFRS and will have a significant impact on both financial statements and the complexity of performing valuations.

Definition

IFRS defines a lease as a contract that conveys the right to control the use of an identified asset for a period of time in exchange for consideration. The right to control is achieved when both the following conditions are met:

a) the customer has the right to obtain the majority economic benefit from the use of the asset; and

b) the customer has the right to direct the use of the asset.

Before IFRS 16 came into effect, almost US$3.0 trillion of off-balance sheet lease commitments were disclosed by listed companies globally using IFRS or US GAAP. The standard was introduced to ensure more faithful representation of a company’s assets and liabilities, with greater transparency about financial leverage and capital employed especially when comparing two separate companies.

Impact on income statements, balance sheets and cashflow

Before IFRS 16, lease costs were recognised as operating costs whereas now they are recognised as finance costs and depreciation charges. Finance costs sit below EBITDA (earnings before interest, taxes and depreciation) on the income statement and operating costs sit above EBITDA.

It’s expected that total lease costs will be higher earlier and lower later in the lease terms, which should result in lower profits earlier in the lease period. However, if a lessee holds multiple leases, starting and ending in different periods, then these fluctuations may even themselves out and the net impact on profit before tax may be neutralised.

Previously lease assets and liabilities were held off the balance sheet in the case of operating leases, IFRS 16s recognition of these lease assets and lease liabilities has changed key ratios such as financial leverage.

IFRS 16 should have no overall impact on cash flow as the increase in operating cash flow should be offset by a decrease in financing cash flow.

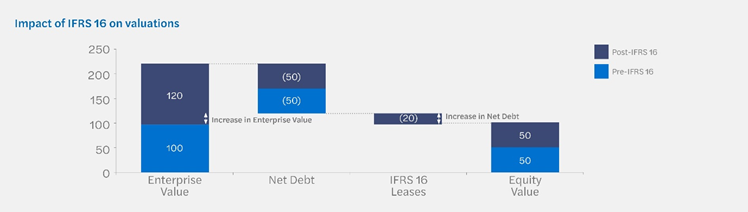

Impact of IFRS 16 on valuations

IFRS 16 increases the implied Enterprise Value of companies which should theoretically be offset by an increase in Net Debt resulting in the same Equity Value.

Although the value attributable to shareholders remains the same, a valuer needs to carefully consider a number of changes to the valuation journey to deal with the impact of IFRS 16.

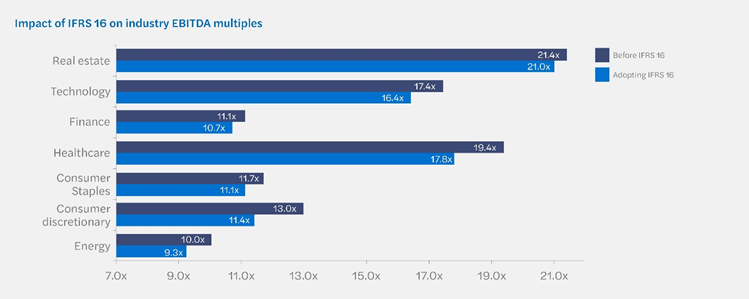

Impact of IFRS 16 on industry EBITDA multiples

IFRS 16 has a significant impact on EBITDA multiples in a range of sectors.

The chart sets out the effect of IFRS 16 on EBITDA multiples for a number of industries by comparing EBITDA multiples before IFRS 16 with EBITDA multiples after adopting IFRS 16.

The chart demonstrates the following:

- The average decrease in EBITDA multiples following the adoption of IFRS 16 is 6.9%; and

- The largest decrease in EBITDA multiple is experienced by the consumer discretionary industry, which includes retail, with a reduction of 14.0%. This may be explained by operators in the sector holding material property leases.

Clearly, these changes can have a significant impact on the outcomes of the valuation performed using the Market Approach if an appropriate adjustment is not applied to ensure that multiples based on comparable assets are viewed on a comparable basis subject to the companies being valued.

Conclusion

In conclusion, IFRS 16 has increased the complexity in performing certain valuations, increased lease assets and lease liabilities on balance sheets and increased the EBITDA of companies holding leases.

For companies that operate in industries that previously had material off-balance sheet lease commitments before adopting IFRS 16, it has caused significant changes to key financial metrics such as leverage, return on investment capital and valuation multiples.

IFRS 16 has not changed the value attributable to shareholders but it has impacted Enterprise Value and Net Debt, valuers must carefully consider these changes when performing a valuation.

Get in touch

If you’d like to know more about IFRS 16 and how it may affect you and your business, please get in contact with your usual contact.

National contacts

Stephen Skeels Partner - Global Head of Valuations

Valuations

Understanding the value of business decisions.