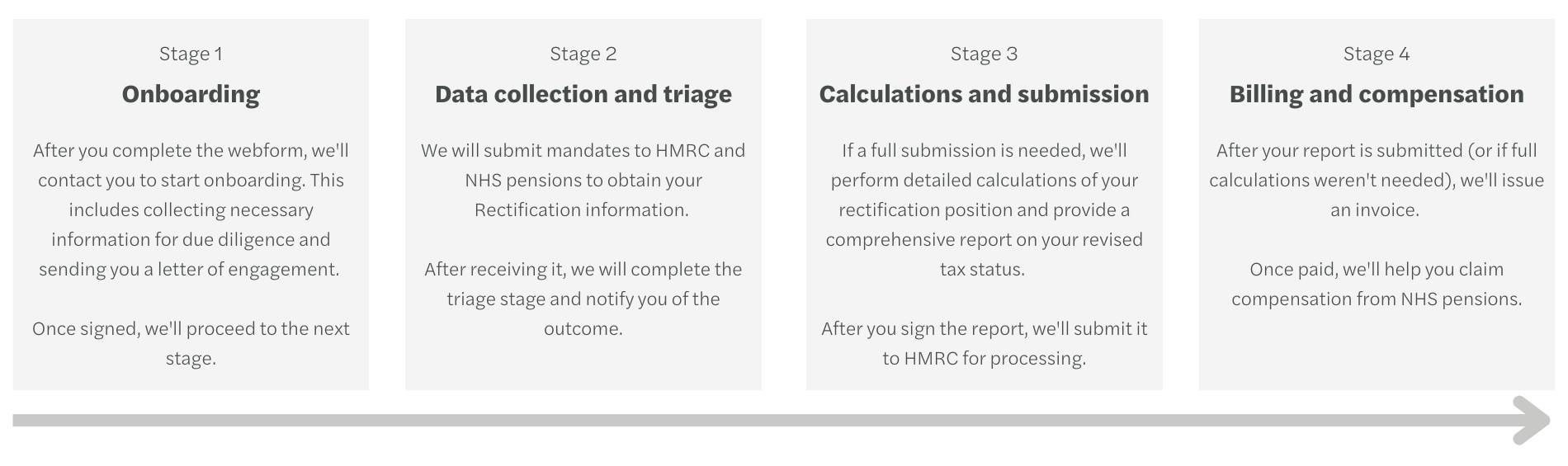

Stage 1: Onboarding

Once you’ve registered your interest with us, our dedicated team will provide further information about our service. Once you are happy to proceed, we will start the process of onboarding you as a client and request that you send us your RPSS statement – The onboarding process will involve gathering certain personal details to complete necessary due diligence checks. Once these are completed, we will issue you with a letter of engagement for signature.

Stage 2: Data collection and triage

Once a client, we will ask you to sign mandates so we can request detailed data from HMRC and NHS pensions. Once the data is received, we will complete calculations to establish if you need to complete a full submission to HMRC – We’ll provide you with the outcome and move to the next stage.

Stage 3: Calculations and submission

If a full submission is required, our dedicated team will complete comprehensive calculations using the data from HMRC and NHS pensions. These will establish the changes in pension growth and assess any revised pension tax charges. This may result in a refund, or in some cases, an additional tax liability.

Once our calculations are complete, we will present you with the results in a comprehensive report. The report will summarise your income and pension position for the affected period, clearly show any refunds or payments due and advise how these are to be paid to you, or to HMRC.

Once you’ve reviewed your report and are satisfied with it, we will submit the outcome to HMRC.

Stage 4: Billing and compensation

After submission to HMRC, our dedicated team will issue you with an invoice for the work completed. Once this is paid, we will support you to reclaim the costs via the NHS cost claim back scheme.

FAQs - all about our process

How does the Rectification process work and what do I receive from you?

The flow chart below shows the full process.

We request info from HMRC and the Pensions Agency. After initial calculations, we inform you if a full HMRC submission is needed.

If so, we complete further calculations and provide a report detailing changes in your pension and any payments or refunds. Our fees are covered by the NHS cost claim back scheme.

How long will it take to complete my McCloud Remedy calculations and receive your report?

Reports are provided within 8 to 10 weeks, depending on sign-ups and info from HMRC and the Pensions Agency. Our team will keep you updated and agree on a report issue date near the end of the process.

What are your charges for McCloud Remedy support?

Charges vary:

Triage only: £240 including VAT (reclaimable from NHS).

Full submission: £1,000 including VAT (reclaimable from NHS).

I’ve completed your web-form, what happens next?

We review your form and start the onboarding process, which can take up to two weeks. Then, we request data from HMRC and the Pensions Agency on your behalf.

Why do I need an accountant? Can I not complete the submission myself?

The HMRC submission is available to anyone, but the process is complex and time-consuming. As tax and pension experts, we review the data from HMRC and NHS pensions, calculate the implications of the McCloud Rectification on you and provide a report of our findings. We guide you through the process for peace of mind.

Wasn’t the deadline for submission supposed to be 31 January 25?

HMRC's deadline is the later of 31 January 25 or 3 months from your RPSS date. Many pension members haven't received their RPSS yet. We do not believe HMRC’s view is to charge interest or penalties given the complexities of the calculations and volume of submissions.

What are contingent decisions and how do they affect me?

Because of the change in pension rules after 1 April 2015, from your legacy pension scheme to the 2015 pension scheme, you may have made decisions in respect of your pension membership (such as opting out or ending additional pension arrangements). Due to the McCloud ruling, such decisions can now be reviewed and potentially altered retrospectively, allowing you to reinstate pension service or similar, should you wish. Our specialist financial planning team can model the implications of this, including the long-term costs/benefits, and advise on outcomes which suit you best.

Do you provide other services and if so, can I speak to someone about them?

As specialist medical accountants and members of AISMA (Association of Specialist Medical Accountants), we provide a range of services to the medical profession. From tax return compliance and advice to GP practice and PCN accounts. We also offer a range of advisory services, including budgeting and forecasting for GP practices.

We have an in-house Financial Planning team who can provide support and advice in relation to the Annual Allowance, Lifetime Allowance and various options to forecast retirement benefits.

If you want to find out more, please email Kieran Hancock (Kieran.Hancock@mazars.co.uk) or Laura Clarkson (Laura.Clarkson@mazars.co.uk).

How to access our NHS McCloud Remedy support

There is concern in the sector that, given the short timescales, a large number of members will all be seeking to access services at the same time. If you have received a “brown envelope” or RPSS you are strongly advised to complete our initial contact form to express interest with no commitment.

Our medical accounting team can assess if you need to use the full HMRC service, help obtain the detailed required information needed for the calculations and complete the HMRC Digital Service on your behalf to make sure that you have correctly declared any amended tax charges. The Government have confirmed it will compensate you for the charge of using our service if you need to use the full Digital Service.

By providing clear, simple steps, we can support NHS professionals to make informed decisions about their pension arrangements. This service is designed to support you every step of the way, ensuring you get the financial compensation and advice you deserve.

Please register for our service, and our team will be in touch with the next steps.

FAQs - everything you need to know about the NHS McCloud Remedy

When is a full submission to HMRC required?

If you have previously paid pension tax charges, or your pension growth for the 2022/23 year is in excess of £40,000, you will need to make a full submission to HMRC.

Why is the McCloud Remedy important?

This ruling is important as it could potentially change the tax position in the remedy period and could result in tax repayments being due. It will change the annual allowance tax position for any impacted member who paid taxes (either via self-assessment or via scheme pays) during the remedy period. For the vast majority of NHS scheme members who paid annual allowance tax, their annual allowance charge will go down and they should be due tax repayment. But they will only get this if they claim.

Please note there could be some cases where the tax charges increase and there will be additional tax payments due.

The ruling will have an impact on future pension decisions as there will be the option of what scheme to include the remedy period service in.

Who is impacted?

Those impacted by the ruling include members of the 1995 or 2008 scheme as of 31 March 2012, who were moved to the 2015 scheme at some point between 1 April 2015 and 31 March 2022.

How do you know if you are impacted?

If you fall into the above category, you will be impacted by the McCloud ruling. If you were a higher earner you should receive a ‘brown envelope’ containing a Remedial Pension Savings Statement (RPSS) detailing the updated pension input amounts for the relevant years.

To access any tax repayment, the annual allowance position will need to be reassessed for that seven year period, and also the 22/23 tax year which was delayed due to McCloud. Instead of resubmitting tax returns for those eight years, HMRC has designed a Digital Service to check calculations and apply for any tax adjustments.

However, the tool is cumbersome, and complex, and can run to over 200 pages for some members, therefore the Government have set up a compensation scheme that can be applied for to potentially cover the cost of having a professional advisor assist you in completing the calculator.

What do those in the NHS affected by the McCloud ruling need to do?

Once an RPSS letter is received, it is important to check if anything needs to be declared to HMRC. All members who previously paid pensions annual allowance tax during the remedy period will need to use the full service - this is because in all cases the annual allowance will change and for the vast majority it will go down. This needs to be reported via the HMRC Digital Service via your Government Gateway account, or via an agent submission on your behalf. You may also be able to claim additional costs - for example, if you paid for financial advice in a certain year, and your charges disappear in that year, clearly you may not have sought pension tax advice in this year.

What could happen if you do nothing?

As noted above, the vast majority of NHS members will find previous annual allowance chances will decrease, and in some cases disappear altogether. However, if you do not claim this, you will forgo the chance to claim tax repayment.

What happens next for those close to retirement?

Your next McCloud choice will not be needed until you retire when you can decide whether you want those seven years in the old final salary legacy scheme or the new reformed 2015 scheme. Again, there is a compensation scheme in place which can be applied for to cover the cost of professional advice to help you.

Revisiting your pension choices

In 2015, most public sector pension schemes, including the NHS Pension Scheme, underwent reforms and, as a result, many members had to transition into new arrangements.

McCloud Judgment – the NHS Cost Claim Back Scheme

A large number of NHS consultants, GP’s, and other scheme members were required to transition to the 2015 scheme in the years from 2015 to 2022. Following a lengthy court process this was deemed discriminatory against younger unprotected members in what has come to be known as the McCloud judgment.

Key contacts

Laura Clarkson Partner – Head of Healthcare - Edinburgh

Kieran Hancock Director - Healthcare - Bristol

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.