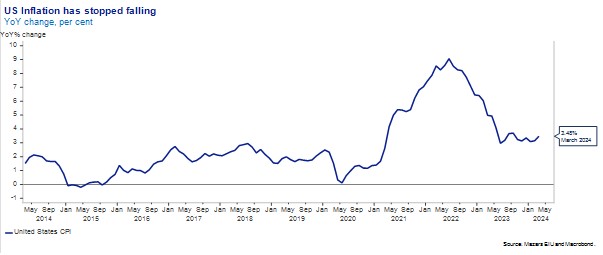

When the US CPI print came in for March at 3.5% it confirmed a trend of three consecutive US inflation numbers coming in above expectations.

The prevailing market narrative up to that point had been that the inflation number was gradually converging with the Federal Reserve’s 2% target and interest rate cuts would come in 2024. Now, the inflation number taken in conjunction with strong US growth expectations has cast doubt on the need for the interest rate cuts in the US. As portfolio managers, we have to decide whether we expect interest rate expectations to come down and we ought to lengthen our portfolio interest rate sensitivity (duration), or whether we believe that interest rates will stay elevated and ought to keep duration low. At our last Investment Committee we lengthened duration, believing that now was a prudent time to increase interest rate sensitivity; this article discussed the question and how we came to our decision.

A look beneath the US inflation number tells us that rising inflation in the US economy is not experienced evenly across all items. In fact, sticky inflation is concentrated in shelter, medical costs and auto insurance and once you strip out these categories US CPI is below 2%. While it isn’t right to pick and chose which sectors to consider as part of the inflation number, it does lead us to question whether this speaks of generally rising prices in the US economy. There is an argument that auto insurance and shelter costs are somewhat backward looking and reflect that car prices and rents have already gone up and thus they do not herald further upward cost pressures down the line. Therefore, to some degree we did not take the rising inflation number in the US at face value.

Another argument for betting against resurgent inflation is that robust US economic growth is not felt evenly across the economy and smaller company surveys show of a lack of optimism for their businesses over the coming year. Purchasing Managers Indices (PMIs) show a recovering manufacturing sector and expanding services sector, but this only reflects large companies, and so we are witnessing a 2-speed economy. It is hard to be certain about the cause of this gap in prospects, but access to finance can explain it to some degree. Small companies tend to borrow for shorter periods of time, exposing them to shorter-term interest rates which are higher than longer term rates while the US yield curve is inverted. Smaller companies financing is also affected by the malaise in commercial real estate. Smaller companies are served by smaller banks, whose loans on CRE make up a higher proportion of their assets compared to larger financial institutions. Historically, small businesses have been a key source of employment in the US and so a retrenchment of spending among smaller companies could have a detrimental impact on employment. A downturn in employment would not support rising inflation.

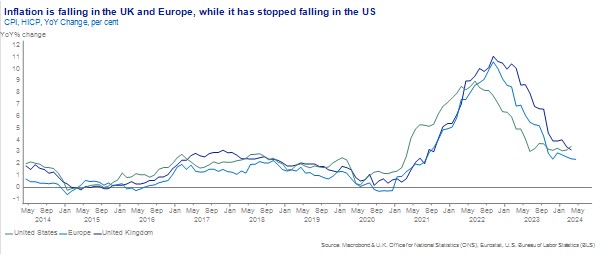

The final point for taking on duration is the uneven economic fortunes that we are seeing across developed markets. The US has experienced healthy growth in 2023 and is forecast to have another year of growth above 2% in 2024. By contrast, the UK was in recession in the second half of 2023, and within Europe a number of countries experience flagging economies, including France and Germany. In 2024, the IMF expects the UK and Europe to grow 0.5% and 0.9% respectively. In the UK there is ample evidence from economic data releases which support that GDP will remain sluggish in 2024: weak retail sales, stalling house price recovery, low consumer confidence, high number of business insolvencies. This economic growth differential between the UK and Europe on the one hand, and the US on the other means that there is a likelihood of the ECB and BoE moving first to cut interest rates. There is a rationale for taking on duration in GBP or Euros which is not present in USD.

The UK and Europe are not experiencing the same economic growth as the US

IMF Economic Estimates/Forecasts, per cent

2023 estimate

2024 forecast

United States

2.5

2.1

Euro Area

0.5

0.9

United Kingdom

0.5

0.6

We opted to add duration in our portfolios at the last Investment Committee, which has been up for discussion for at least 9 months. We felt that the market’s lurch to accept that interest rates would have to remain high was excessively pessimistic and that bond yields were high on an absolute basis and so created an attractive entry point. While interest rates remaining high is a possibility, we still feel that on balance of probability the next move will be downwards. Therefore, we opted to position for the eventual fall in yields at this point. We also split our exposure between US and UK government bonds, thus we are diversified across the inflation stories of 2 regions.

Written by James Hunter-Jones, Associate Director, Financial Planning

Global equity markets entered 2024 with significant momentum from the last two months of 2023 fueled by falling inflation and hopes of lower interest rates during the year. Despite a fast reduction of rate cut expectations in 2024, from 7 to 2 (and even possibly none) in the US, and persistent Quantitative Tightening, equities carried the momentum forward, gaining 7.5%, a full year’s return on the...

Since the beginning of the pandemic, global stock markets have gained +48%. At the same time, the US stock market has increased its capitalisation by 69%, led by the tech sector which more than doubled in value, gaining 134%. Those numbers come against a backdrop of lockdowns, trade wars, broken supply chains, below-trend economic growth, high inflation and fairly restrictive monetary policy. Ex-technology,...

A whole generation of investors who started their careers in the post-Global Financial Crisis (GFC) period have only experienced returns for emerging market (EM) equities which look like this: