1. What are the benefits of conducting climate scenario analysis?

Conducting a climate scenario analysis enables organisations to understand how their current business model and supply chain will hold under different future climate situation. This gives organisations an opportunity to adjust their strategy and business model to become more climate resilient and seize future market opportunities.

2. Why should I report climate scenario analysis?

Reporting the results of the climate scenario analysis is required under IFRS S2 and AASB S2. Besides, these results provide useful insights for investors to assess the climate resilience and adaptation of a business.

3. What is climate adaptation?

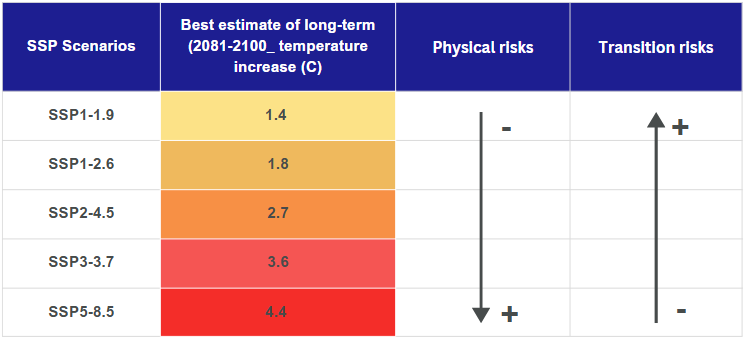

Climate adaptation refers to a business's capacity to prevent financial losses caused by climate change. Actions could include adjusting the current business model, developing innovative solutions minimise potential effects of floods, drought, etc or explore market opportunities offered by the green transition.

4. What is climate mitigation?

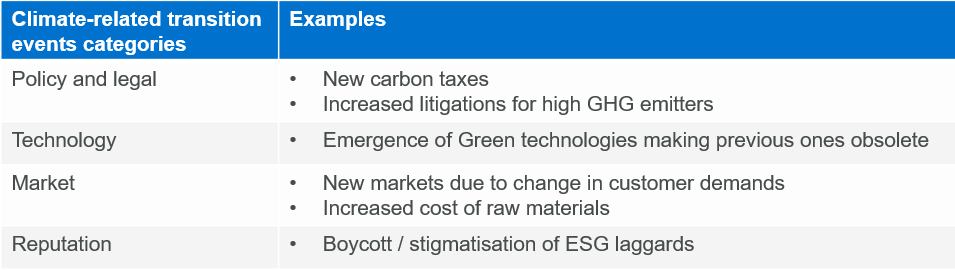

Climate mitigation means contributing to lowering greenhouse gas emissions in the air. For businesses, this involves taking actions to reduce their scope 1, 2, and 3 emissions.

5. What is climate resilience?

Is characterised by the ability for a business to anticipate, plan for and respond to climate related events and changes. The way to improve your resilience is making more decisions in the present to mitigate the climate-related risks and take action to respond to these now for less detriment in the future.

How Forvis Mazars can help

- AASB S2 gap analysis and detailed implementation action plan / roadmap

- Carbon footprint calculations and analysis

- Decarbonisation pathways and target setting

- Review of governance arrangements around climate risks and opportunities

- Physical and transition risks and opportunities analysis

- Climate scenario analysis

- Risk management and internal control development and implementation

- Reporting assistance

Date published: 05/11/2024

Please note that this publication is intended to provide a general summary and should not be relied upon as a substitute for personal advice.

All rights reserved. This publication in whole or in part may not be reproduced, distributed or used in any manner whatsoever without the express prior and written consent of the Forvis Mazars, except for the use of brief quotations in the press, in social media or in another communication tool, as long as Forvis Mazars and the source of the publication are duly mentioned. In all cases, Forvis Mazars’ intellectual property rights are protected and the Forvis Mazars Group shall not be liable for any use of this publication by third parties, either with or without Forvis Mazars’ prior authorisation. Also please note that this publication is intended to provide a general summary and should not be relied upon as a substitute for personal advice. Content is accurate as at the date published.

Sustainability

Helping companies place sustainability at the centre of their business.

ESG reporting Australia

Mandatory climate reporting has been introduced in Australia. To meet AASB S2 requirements, learn about the Australian sustainability reporting standards and the climate related financial disclosures regulation.

ESG learning centre

This section covers the basics of sustainability. For instance, what is ESG, how climate change affects businesses, what is carbon accounting, how AASB S2 differs from IFRS S2, what are climate scenarios?

Want to know more?

Jim Mascitelli Partner - Sydney

Contact us

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.