In September 2024, mandatory climate reporting was introduced in Australia, requiring companies to include a sustainability report in their annual report. More than 6,000 entities will have to comply with this regulation.

The sustainability report shall include a climate statement prepared in accordance with AASB S2 Climate-related disclosures and audited annually.

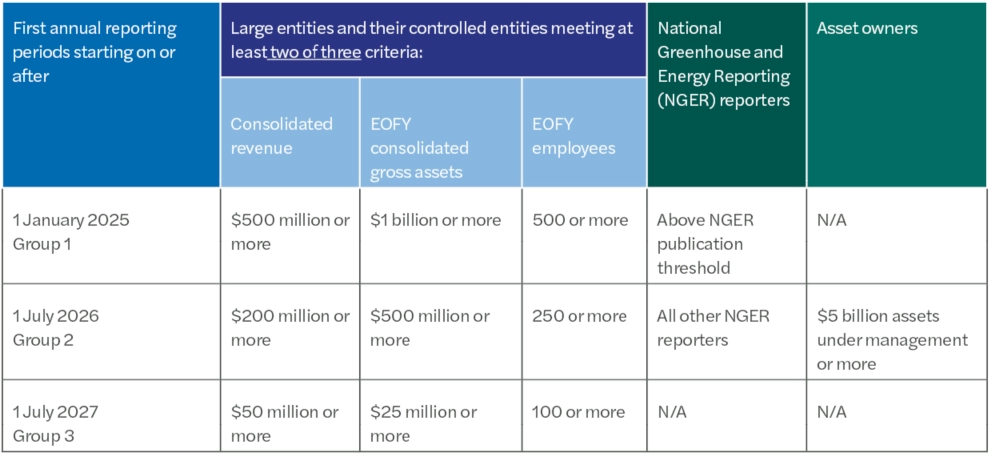

Mandatory climate reporting applies to companies meeting the criteria set in the below table. If not falling under these criteria, the business is exempt from mandatory reporting.

Figure 1

What are the Australian Sustainability Reporting Standards (ASRS)?

In September 2024, the Australian Accounting Standards Board (AASB) issued the ASRS on disclosures of climate-related financial information. These standards build upon the international financial reporting standards (IFRS) Sustainability Disclosure Standards (SDS) issued by the International Sustainability Standards Board (ISSB). It adopts the four-pillar structure (Governance, Strategy, Risk Management, Metrics and Targets) from the Task Force on Climate-related Financial Disclosures.

The Australian Sustainability Reporting Standards (ASRS) include two standards:

AASB S1 General Requirements for Disclosure of Sustainability-related Financial Information builds upon IFRS S1 and is a voluntary standard in Australia.

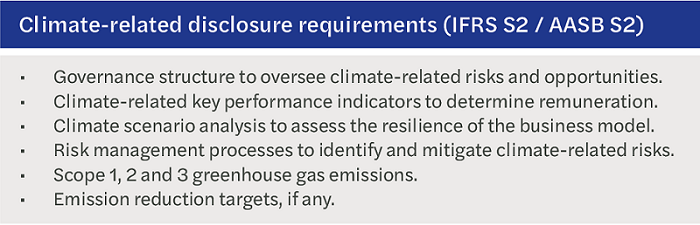

AASB S2 Climate-related Disclosures builds upon IFRS S2 with a few adaptations for Australia and is mandatory for companies meeting the criteria. Our Climate reporting readiness tool and our ad hoc research report provide further information on the AASB S2 requirements. Figure 2 highlights a few requirements of IFRS S2 / AASB S2.

Figure 2

How does Australian standards differ from international standards?

ASRS and IFRS SDS share many similarities but there are a few differences.

IFRS SDS require IFRS S1 (that deal broadly with sustainability-related risks and opportunities) and S2 (specific to climate-related risks and opportunities) to be applied together. In contrast, the AASB has decided to make IFRS S1 a voluntary standard and integrate some part of IFRS S1 (relevant concepts and definitions) to make AASB S2 a standalone standard.

Other notable differences are:

In AASB S2, references to SASB have been deleted. The AASB will reconsider that decision once work to internationalise SASB standards have been finalised.

While IFRS S2 does not specify the number of scenario and the scenario to be used by companies, the amended Corp Act 2001 requires companies to consider two climate scenarios, a high global warming scenario (2.5°C or higher) and a low global warming scenario (1.5°C above pre-industrial levels).

What is the content of the sustainability report?

The sustainability report shall include:

a climate statement prepared in accordance with ASRS, specifically aasb s2 climate-related disclosures;

notes to the climate statement (if any);

any statements required a legislative instrument by the Minister relating to matters concerning environmental sustainability; and

the directors’ declaration about the statements and notes.

Broadly, the climate statement shall include a description of:

the governance structure to oversee climate-related risks and opportunities,

scope 1, 2 and 3 GHG emissions using the GHG protocol (or NGER Legislation Scheme for scope 1 and 2 emissions if the company is subject to it).

Decarbonisation targets if the company has decided to set targets to reduce its scope 1, 2 and/or 3 emissions.

What is the timeline for assurance of sustainability information?

On 29 January 2025, the AUASB approved the Australia Sustainability Assurance Standard ASSA 5010 Timeline for Audits or Reviews of Information in Sustainability Reports under the Corporation Act 2001. As a first step, limited assurance will be mandatory on selected parts of the report (Governance, Strategy -risk and opportunities, and scope 1 and 2 Emissions). Reasonable assurance on the full sustainability report will then be required for all companies in the scope of the regulation for the period starting 1st July 2030. Figure 4 describes the timeline for assurance approved by the Board of the AUASB.

Figure 3

What are the risks faced by directors in case of non-compliance?

In case of non-compliance, Directors face civil penalties. However, limited immunity for Directors has been introduced in the Corporation Act 2001.

For the first year, only ASIC can take actions in case of incorrect, incomplete or misleading forward-looking statements. Anyone can then bring action against Directors with regards to forward looking statements.

For the first three years, only ASIC can take actions in case of incorrect, incomplete or misleading statements in relation to scope 3 emissions, scenario analysis, and transition plan.

How will ASIC oversee sustainability reporting?

As declared by ASIC Commissioner Kate O’Rourke in Sept 2024, "ASIC recognises there will be a period of transition as organisations develop the capabilities required to comply. We will take a proportional and pragmatic approach to supervision and enforcement as industry adjusts to these new requirements."

The supervision of sustainability reporting will be aligned with on the current annual surveillance program for financial reporting. The annual climate-related disclosures surveillance program will start in 2026 for Group 1 entities and will include a publicly available report of ASIC findings.

What are the benefits of climate reporting?

Beyond meeting compliance requirements, preparing a climate-related reporting can benefit companies in multiple ways.

First, Directors' fiduciary obligations include identifying and understanding risks, including climate risks that may affect the company's prospects. Preparing a climate report would help Directors fulfilling their duty of care and diligence.

Second, the Green transition offers business opportunities as new technologies are arising, customers preferences are changing, new sustainability regulations are introduced... Climate reporting offers the opportunity to business leaders to reflect on their current business model and take a long-term of their business strategy. For instance, a company producing diesel generators may start considering alternative innovative technology as the world is progressively moving away from fossil fuel.

Third, climate reporting can help companies can better future-proof their business. A clear identification of the material climate physical risks and transition risks as well a climate scenario analysis over the short, medium and long-term enable companies to understand weakness in their operations and supply chain. It is then possible for companies to build up climate resilience of their physical assets (e.g., prevention against flood risks) and in their supply chain (e.g., supplier diversification for critical inputs).

Other benefits include:

Enhanced data management

Development of credible decarbonisation pathway

Boost to brand reputation with customers

Attraction of more investments through enhanced transparency and obtain financing at discounted interest rates from banks

What is the TCFD Framework?

The Task Force on Climate-related Financial Disclosures was initiated by the Financial Stability Board (FSB) in 2015 to help companies provide climate-related risks information that meet the needs of investors.

The Task Force published in 2017 a set of 11 recommendations categorised along 4 main pillars: Governance, Strategy, Risk Management and Metrics and Targets.

Many companies around the world have voluntarily reported their climate-related risks in accordance with the TCFD recommendations. In Australia, the recommendation 7.4 of the ASX. Principles and Recommendations issued in 2019 encourages companies to consider disclosing their climate-related risks according to the TCFD recommendations.

1. Which companies must prepare mandatory climate reporting?

Australian companies meeting two of these criteria will have to prepare climate-related disclosures:

- A$ 50+ million consolidated turnovers

- A$25+ million consolidated gross assets

- 100+ employees

Further details on the criteria and timeline are provided in Figure 1.

2. If the parent company overseas has prepared a climate report, does the Australian subsidiary need to prepare a climate-reporting?

Australian subsidiaries won’t be allowed to lodge the consolidated group sustainability report. They will have to prepare and lodge their own sustainability report and climate statement in accordance with AASB S2 if they meet the thresholds detailed in Figure 1.

3. Does climate reporting need to be audited?

For companies required to prepare and lodge a sustainability report that includes a climate statement, this report will have to undergo an external audit process. As per the amended Corporation Act 2001, the company financial auditor with the support of sustainability experts will provide an external audit opinion in accordance with the phasing model defined by the Auditing and Assurance Standards Board (AUASB).

4. What auditing standards are used for verifying sustainability reports?

The AUASB is also in charge of developing the assurance standards that will be applicable for the audit and assurance of sustainability reports. At an international level, in November 2024, the International Auditing and Assurance Standards Board (IAASB) issued ISSA 5000 General Requirements for Sustainability Assurance Engagements. This international standard was approved for use in Australia on 29 January 2025, with AUASB issuing ASSA 5000 General Requirements for Sustainability Assurance Engagements for the assurance of mandatory climate reporting[1].

AASB S2 Climate-related Disclosures builds upon IFRS S2 with a few adaptations for Australia.

- As per the amended Corporation Act 2001 (Subsection 296D(2b), two climate scenarios shall be considered, including a high global warming scenario (2.5°C or higher) and a low global warming scenario (1.5°C above pre-industrial levels).

- AASB S2 incorporates parts of AASB S1 in Appendix D to make AASB S2 a standalone mandatory standard.

6. What are IFRS SDS?

Building upon the TCFD framework, the ISSB issued the IFRS Sustainability Disclosure Standards (SDS).

- IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information. It requires a company to disclose information about its governance, strategy and risk management, as well as metrics and targets, in relation to its sustainability‑related risks and opportunities.

- IFRS S2 Climate-related Disclosures. It extends the TFCD recommendations and requires companies to provide more granular information on their climate-related risks and opportunities.

7. What are the differences between TCFD to IFRS S2 (TCFD Vs IFRS S2)?

For companies already disclosing in accordance with the TFCD recommendations, complying with AASB S2 requirements will require to provide more granular information. The IFRS website outlines that “the requirements in IFRS S2 integrate, and are consistent with, the TCFD’s four core recommendations and 11 recommended disclosures, with minor differences.”

8. What are the differences between TCFD to AASB S2 (TCFD vs AASB S2)

Given the strong alignment between IFRS S2 and AASB S2, most of the differences highlighted by the ISSB apply (see detailed comparison table) and most relate to the need to provide more granular and detailed information. Then, there are also area of differences between IFRS S2 and AASB S2 that would need to be considered to transition from TCFD to AASB S2. For instance, AASB S2, in line with the Australian climate regulation, requires using two climate scenarios, including a high global warming scenario (2.5°C or higher) and a low global warming scenario (1.5°C above pre-industrial levels).

9. Do I have to climate report if my company isn’t meeting the criteria?

No, legally you do not have to. However, your shareholders, customers and other stakeholders may expect your company to report (some) climate related disclosures. It is possible to prepare a voluntary climate report.

10. Is it mandatory to report scope 3 emissions in the first year?

As per AASB S2, para C4(b), companies are not required to disclose scope 3 emissions in the first reporting year.

11. What is SASB?

The Sustainability Accounting Standards Board (SASB) has developed 77 sector specific standards. These standards help companies identify sustainability-related risks and opportunities that are likely to be financially material for them and their peers working in the same industry. Following the merger between SASB and the IFRS Foundation, these standards are currently being revised.

How can Forvis Mazars help:

AASB S2 gap analysis and detailed implementation action plan / roadmap

Carbon footprint calculations and analysis

Decarbonisation pathways and target setting

Review of governance arrangements around climate risks and opportunities

Physical and transition risks and opportunities analysis

Climate scenario analysis

Risk management and internal control development and implementation

Mandatory climate reporting has been introduced in Australia. To meet AASB S2 requirements, learn about the Australian sustainability reporting standards and the climate related financial disclosures regulation.

This section covers the basics of sustainability. For instance, what is ESG, how climate change affects businesses, what is carbon accounting, how AASB S2 differs from IFRS S2, what are climate scenarios?