Goodwill in M&A: Hidden Risks and the Importance of Purchase Price Allocation

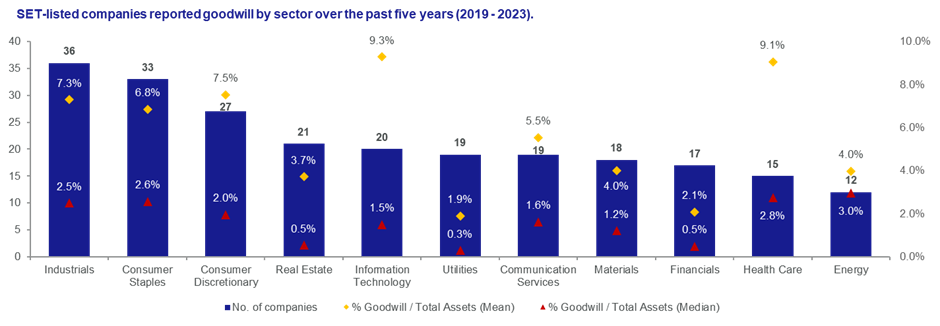

A recent review of Thai-listed companies reveals that 32.5% reported goodwill on their balance sheets over the last five years.

Goodwill arises during acquisitions when the purchase price exceeds the fair value of the acquired company's identifiable net assets, reflecting intangible elements such as brand reputation, customer relationships, and intellectual property. The acquirer must allocate a purchase price for the acquired tangible and identifiable intangible assets and liabilities, in line with IFRS 3, ‘Business Combinations’. Since this allocation is based on the fair value of these assets and liabilities, the acquirer has considerable discretion in allocating the purchase price. Any difference between the purchase price and the fair value of the identifiable net assets is recorded as goodwill.

Source: Capital IQ and Forvis Mazars’ analysis

In 2023, we were engaged by a prominent Japanese-listed conglomerate to review its investment in a Thai management consulting firm. The Japanese company, trading on the Tokyo Stock Exchange for over two decades, is known for its diversified product portfolio and ambitious growth strategies. As part of expanding its engineering consulting business, it acquired the Thai firm, which services infrastructure and oil & gas projects. The Japanese company paid 50% of the M&A transaction value in cash and agreed to settle the rest through deferred payments in an earn-out arrangement. The primary motivation for the purchase was the Thai firm’s impressive client base, which was expected to significantly increase the Japanese conglomerate's revenue pipeline in Thailand.

However, during our review, we noticed several red flags. While the Thai firm had a solid client list, many were non-recurring, and substantial outstanding receivables raised questions about its financial stability. Yet, the Japanese company valued the Thai firm’s goodwill at over 60% of the total M&A transaction price, which warranted deeper analysis. When we assessed the Thai firm's tangible assets, they accounted for just 15% of the total M&A transaction value, suggesting a potentially inflated goodwill valuation. This raised critical questions: Is the Thai company’s goodwill justified? With a non-recurring client base, could the Japanese company realistically recover its investment?

In another case, several years before, we worked with a large Middle Eastern oil company that had acquired an Eastern European firm from an American hedge fund for EUR 2.7 billion. The acquired company claimed to produce a chemical essential to refining petroleum, making the acquisition seemingly ideal. But after three years with no returns, the Middle Eastern company asked us to investigate. Upon visiting the European target, we discovered that it was not producing the chemicals it claimed and lacked the resources and operational capability to do so. This led to a forensic investigation revealing manipulation and fraud in the M&A transaction, which attracted legal attention from the Ministry of Oil & Gas and tarnished the company’s reputation. Ultimately, the company was forced to write off over 75% of its EUR 2.7 billion investment, erasing more than EUR 2 billion in goodwill from its balance sheet and causing significant financial damage.

These cases underscore questions about goodwill: How can goodwill be monitored on the balance sheet? Perhaps more critically, is high goodwill used to obscure potential misappropriations?

Purchase Price Allocation (PPA): The Key to Transparent Financial Reporting

A realistic PPA allocates the acquisition price to identifiable assets and liabilities at fair market value, with any excess recorded as goodwill. Here’s why PPA is critical:

Common Pitfalls related to a PPA

Despite its importance, companies often encounter pitfalls in relation to a PPA, including the following:

Conclusion

Accurate goodwill and intangible asset valuations through a PPA are more than just accounting tasks; they are critical for financial transparency and compliance. Companies that excel in managing goodwill and PPA processes position themselves as trustworthy entities in the eyes of investors. In an era where clear and transparent reporting is paramount, a sound approach to a PPA is essential to maintaining a solid reputation and supporting sustainable growth in M&A transactions.

How we can help

If you would like to discuss this topic in further detail, please get in touch with us.

Want to know more?

Surichai Saeaid Financial Advisory Director - Bangkok