Financial advisory

We provide support for the critical moments that define the success of your business.

Rebuilding credit card profitability post COVID-19

With customers in distress revenue levers are going to be hard to pull, so cost management strategies will need to come to the fore. No doubt tough decisions will need to be made, but care should be taken not to cut too deep and damage future prospects. Wherever possible sustainable efficiency savings should be prioritized over blunt “quick-fix” cuts in areas such as staffing and marketing.

Let’s be clear; efficiency savings are harder to achieve than quick-fix cuts, and may require expert advice. The upside is that they make the organization fitter, more competitive and more robust on an ongoing basis. They are “no-regret” actions.

So how can these savings be obtained? Here we’ll focus on two of the industry’s largest variable cost lines:

Points based reward programs are an important part of the overall credit card proposition. They are used to attract/retain customers and also to incentivise spend. Cost-reduction efforts in this area typically focus on reducing earn rates or increasing the number of points needed to redeem rewards. Whilst both aspects do need to be properly calibrated, these adjustments represent dis-investment in the customer proposition and risk a negative impact in the longer term.

Efficiency gains should be prioritized ahead of cuts and can be achieved in a number of areas including:

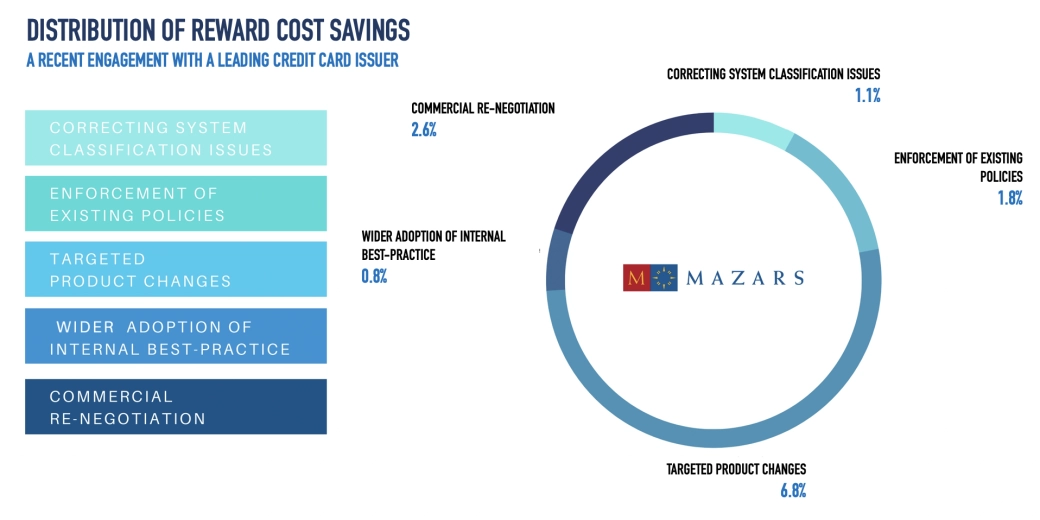

A well-executed efficiency program can often reduce cost by 10-15% without impacting the customer proposition or market competitiveness. The chart below illustrates the sources of cost savings from a recent engagement with a major card issuer where savings worth circa 13% of total reward costs were identified.

Every time a credit, debit or prepaid card is used both the issuing bank and acquiring bank pay a small fee to the card scheme with which the card is associated (typically Visa or Mastercard). With huge numbers of transactions these fees quickly mount up to significant values and it is no surprise that both Visa and Mastercard are highly profitable organisations. So what can be done to contain or reduce these costs?

Leading banks in North America, Europe and Australia have taken steps to reduce these costs and have achieved significant savings. In general Asian and African banks have not been as active in managing this aspect of their businesses, so what can they learn from their Western counterparts?

Generally the banks that have made progress in this area have focused on the following:

In summary, issuers can act now to increase cost efficiency in ways that do not involve reducing staffing levels. Doing so is a “no-regret” action and should be considered before reducing investment in growth or customer service initiatives. Both areas are highly technical and obtaining expert advice, especially at the start of an initiative is likely to yield better results.

We provide support for the critical moments that define the success of your business.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.