Key points on Pillar 2: 15% tax rate

Finance (No. 2) Act 2023 included legislation for the implementation of Pillar Two and the minimum effective tax rate of 15%,in Ireland.

These changes have been broadly welcomed and signal the government's continued support for businesses of all sizes engaged in Research & Development (R&D). The increase R&D tax credit rate and the increase in the level of the first instalment are very welcome measures, while the pre-notification requirement introduces an additional administrative requirement which will affect some claimants, particularly start-ups.

The changes outlined below will apply for accounting periods commencing on or after 1 January 2024.

The Bill outlines an increase in the RDTC rate from 25% to 30%. This adjustment is designed to uphold the net benefit for large organisations (those with a group turnover exceeding €750m) while enhancing the credit's value for SMEs.

Claimants of the RDTC will continue to have the option to:

Many loss-making or pre-revenue claimants will continue to opt for refundable instalments, serving as a crucial source of innovation funding.

The refundable instalments will now be payable as follows:

1) The first instalment is the greater of:

2) The second instalment will continue to be based on three fifths (30%) of any balance of the remaining R&D corporation tax credit, and

3) The third instalment will continue to be any balance of the R&D corporation tax credit remaining (20%), being the credit claimed less the first and second instalment amounts already claimed.

*This had previously been €25,000.

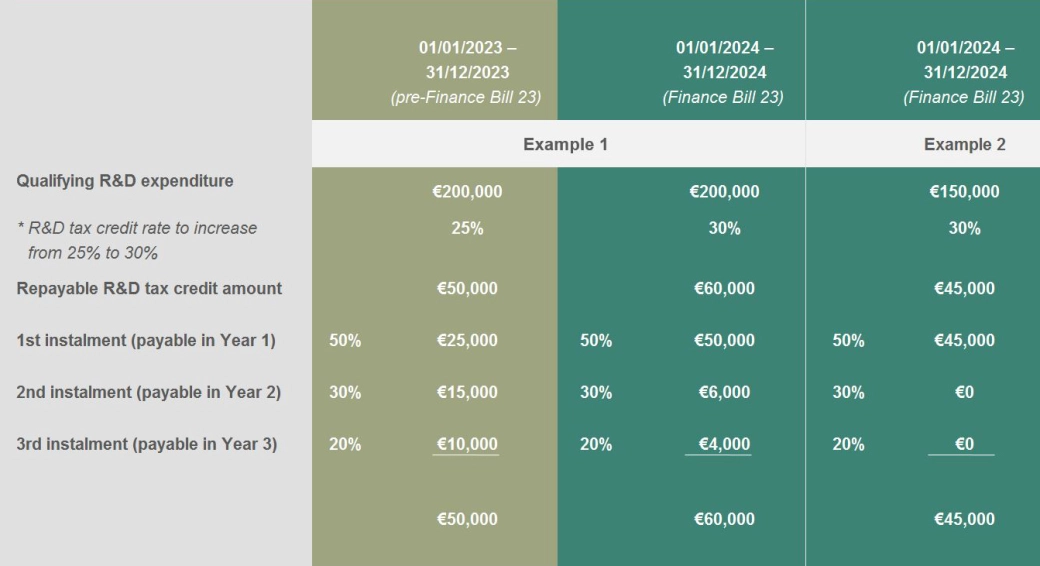

To illustrate the impact of the new 30% rate and the increased pay-out limitation for the first instalment, we provide examples in the table below:

As demonstrated in Example 1, an R&D expenditure of €200,000 in 2024 results in claimants receiving an RDTC of €60,000, with €50,000 payable in Year 1. This marks a significant increase from the €50,000 credit applicable for 2023, with only €25,000 payable in Year 1 for the same level of R&D spending.

In Example 2, an R&D expenditure of €150,000 in 2024 enables the claimant to receive the full benefit of the tax credit in Year 1 since the credit is less than €50,000.

The Bill stipulates a pre-notification obligation for claimants who haven't claimed the RDTC in any of the preceding three accounting periods leading up to the period for which they intend to claim. The mandatory details include:

This pre-notification must be submitted at least 90 days before filing a claim, with similar rules now extending to claims related to R&D buildings.

The RDTC must be claimed within 12 months of the end of the accounting period. Therefore, a claimant with a 31 December 2024 accounting period has until 31 December 2025 to claim the RDTC. A company who has not filed an RDTC claim in any of the preceding three accounting periods will need to notify Revenue of their intention to do so on before 30 September 2025, otherwise the opportunity to claim the RDTC will be lost.

Finance (No. 2) Act 2023 included legislation for the implementation of Pillar Two and the minimum effective tax rate of 15%,in Ireland.

Angel investors are entitled to a reduced tax rate on the capital gains when the Finance Act 2023 came into effect in December 2023. Here are the main points regarding this new relief that you may be able to take advantage of.

If you had a homeowners mortgage with a balance of between €80,000 and €500,000 as of 31 December 2022 and were hit by interest rate hikes in 2023, then you may qualify for a tax credit of up to €1,250 per property.

Insight and innovation to guide you through an ever-evolving tax landscape.

A global approach that maximises tax benefits

Strategies and solutions to help you stay compliant in an evolving environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.