Definition of single-purpose vouchers - ECJ ruling of 18 April 2024, C-68/23

ServicesTaxGlobal Indirect Tax - Value Added Tax and CustomsLatest VAT News

Definition of single-purpose vouchers

Since 1 January 2019, vouchers are handled the same throughout the EU, and how a voucher is treated depends on whether it is a single-purpose or multi-purpose voucher. In the case of chain transactions involving vouchers, the question arose as to the impact of uncertainties regarding the taxation of upstream transfers. The ECJ answered this question following a referral from the BFH (German Federal Fiscal Court).

Facts of the case

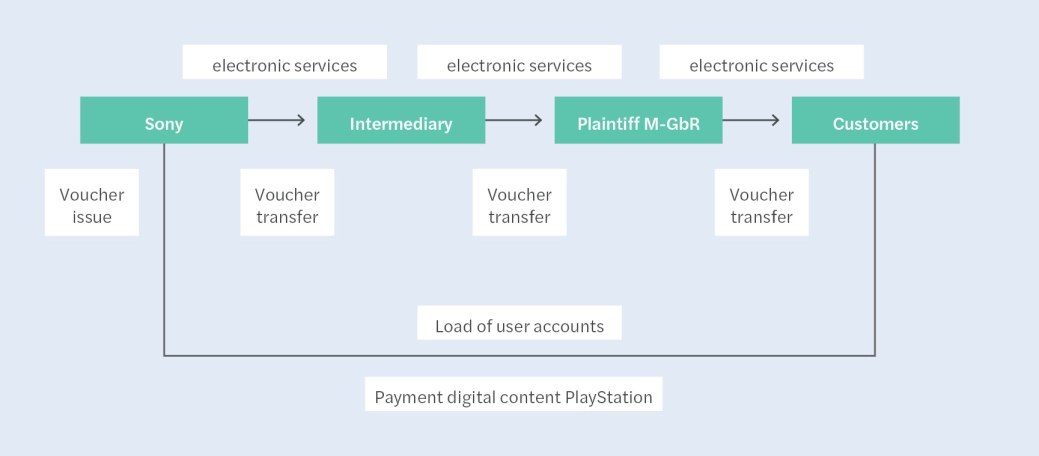

The plaintiff traded in voucher codes for the purchase of digital content for the PlayStation Network, so-called PSN Cards. These PSN Cards were issued by Sony Europe, a company based in the United Kingdom. PlayStation customers could use these codes to top up their customer account with Sony and then use this credit to purchase digital services. Sony transferred these voucher codes to intermediaries based in various EU Member States, who in turn transferred them to the plaintiff M-GbR. The latter then transferred them to PlayStation customers via an online store.

When customers set up a customer account with Sony, they were asked for their place of residence. German customers then received a German customer account. The PSN voucher codes also had country codes. PSN Cards with the country code "DE" could only be redeemed for German customer accounts. The terms of use expressly obligated the customer to be honest in their use. These measures were intended to ensure that when a PSN Card with the identifier "DE" was issued, it was clear that only customers resident in Germany could use the PSN Card. In reality, price differences led some customers to occasionally (improperly) register in a country other than their country of residence.

Questions referred and the answers

The BFH initially assumed that although some customers occasionally acted in breach of contract, the plaintiff could, in principle, assume that the customers were indeed resident in Germany.

The first question referred

However, the question was whether, at the time the PSN Cards were issued, the place of supply of the services for which the voucher had been obtained – and the VAT due on these services – had already been determined, so that it is a single-purpose voucher within the meaning of Art. 30a No. 2 of the VAT Directive. In this case, all the traders involved in the chain would have provided a fictitious electronic service as per Art. 30b para. 1 of the VAT Directive. Otherwise, there would have been a multi-purpose voucher within the meaning of Art. 30a no. 3 of the VAT Directive, meaning that the transfer transactions would not be subject to VAT, but the final service actually provided would be.

As the PSN voucher codes were already labelled with a specific country code at the time they were issued, the place of supply to the customer in this case was determined when the voucher was issued. If it is assumed that they are generally resident in Germany, the place of supply is in Germany in accordance with § 3a (5) sentence 2 no. 3 UStG (German VAT Code), respectively Art. 58 No. 1 lit. c VAT Directive. With regard to the place of supply for the electronic services provided by Sony to the intermediaries, the BFH raised the question in its order for reference as to whether the place of supply in relation to the end customer (Germany) also automatically applies to all upstream transactions or whether the place of supply should be assessed individually and be located at the place of establishment of the respective intermediaries in accordance with § 3a (2) UStG, respectively Art. 44 VAT Directive. In the latter case, the place of supply in this relationship would not be determined when the voucher was issued because the intermediaries were based in different countries. Accordingly, the question arises as to whether the place of supply for a single-purpose voucher only has to be determined for the supply to the customer or for all upstream transactions as well.

The ECJ agreed with the BFH in its assessment that the place of supply to the customer can be considered to be in Germany despite occasional abuse.

The Federal Fiscal Court did not formulate the (preliminary) question of whether the place of supply of the transfers must be assessed individually as a question for reference. Accordingly, the ECJ did not answer it explicitly but apparently assumed that the place of supply for the electronic service from Sony to the intermediary had not yet been determined – which implies that an individual assessment must be made and § 3a (2) UStG must be applied.

The court stated that only the place, and taxation of the service to the customer, must be determined at the time of issue. If this were also required for all upstream transfers of the voucher, the scope of application of single-purpose vouchers would be extremely restricted. This is not the purpose of the regulation introduced in 2019, according to which the multi-purpose voucher has a catch-all function. In addition, the voucher regulations should be constructed in such a way as to provide legal certainty, especially for scenarios in which vouchers are transferred multiple times. This objective cannot be achieved if international cases such as the present one are excluded from the scope of application of the single-purpose voucher.

The second question referred

If the ECJ were to assume a multi-purpose voucher in the present case, the ECJ asked whether taxable distribution or promotion services pursuant to the second subparagraph of Art. 30b (2) of the VAT Directive were present or whether the principles of the ECJ case "Lebara" should be applied. Lebara was a telephone company which, in 2005 (i.e. long before the Voucher Directive came into force), sold telephone cards to intermediaries in various EU Member States, who in turn resold them to end consumers in the same Member State. The ECJ ruled at the time that Lebara had supplied telecommunications services to the intermediaries; the prepaid cards were treated as goods. For the BFH, the relationship between this judgement and the voucher regulations in their current form seemed unclear.

Here, the ECJ limited itself to the answer that taxable distribution or promotion services were conceivable, but that the BFH would have to examine this. In any case, the "Lebara" judgement was irrelevant as it concerned a situation before the Voucher Directive came into force. According to the current legal situation, the telephone cards in the Lebara case would be single-purpose vouchers.

Practical implications

The ECJ's decision has clarified the distinction between single-purpose and multi-purpose vouchers.

The classification of the voucher as a single-purpose voucher means that the transfer of this voucher is deemed to be a supply of the goods or provision of the service to which the voucher relates.

The question could, however,be asked: What does this judgement mean with regard to determining the place of the upstream transfers? The ECJ and BFH implicitly assume that the place of the upstream supplies does not necessarily correspond to the place of supply to the end customer. In our view, this is logical, as it corresponds to how other supply (chain) fictions are handled. However, a clarification would have been desirable.

If the place of supply of upstream transfers is not automatically apparent, it means that increased attention must be paid to the VAT status, place of business, any permanent establishments, and the question whether the supply of services is destined for the permanent establishment.

The BFH and ECJ were magnanimous regarding the question of whether the place of supply for services to German customers is Germany despite the occasional misuse when the voucher is issued. However, this decision relates to a specific individual case and should not be generalised. In principle, great care should be taken when ensuring the place of residence and, where applicable, the potential VAT status of customers.

Author

Nadia Schulte

Tel.: +49 211 83 99 330

Want to know more?

Birgit Jürgensmann Partner - Düsseldorf

Thomas Pelzer Partner - Berlin

Stephanie Stahl Senior Manager - Berlin