BFH decision XI S 4/21 involves the requirements for a single-purpose voucher in the case of chain transactions

ServicesTaxGlobal Indirect Tax - Value Added Tax and CustomsLatest VAT News

BFH XI S 4/21 transactions single-purpose vouchers

With retroactive effect to 1 January 2019, the German legislature has transposed the EU Voucher Directive into national law. In section 3.17 of the VAT application decree, the German tax authorities provide a detailed statement. However, questions still remain. The BFH (Federal Financial Court) has now granted a suspension of execution with regard to a chain transaction with (alleged?) single-purpose vouchers.

Background: New voucher regulation in § 3 (14) and (15) of the UStG (German VAT Code)

Under the new legislation, a distinction must be made between single-purpose and multi-purpose vouchers. A voucher for which the place of the supply of goods/services to which the voucher relates and the VAT due on these transactions are known at the time the voucher is issued is a single-purpose voucher. When the voucher is transferred or issued, the respective entrepreneurs shall pay VAT on a turnover corresponding to the supply referenced in the voucher. Vouchers that do not meet these requirements are considered multi-purpose vouchers. In this case, the transfer or issuance is not a transaction subject to VAT. Only the supply actually rendered, which the voucher entitles the holder to receive, is subject to VAT.

Facts of the Financial Court judgement

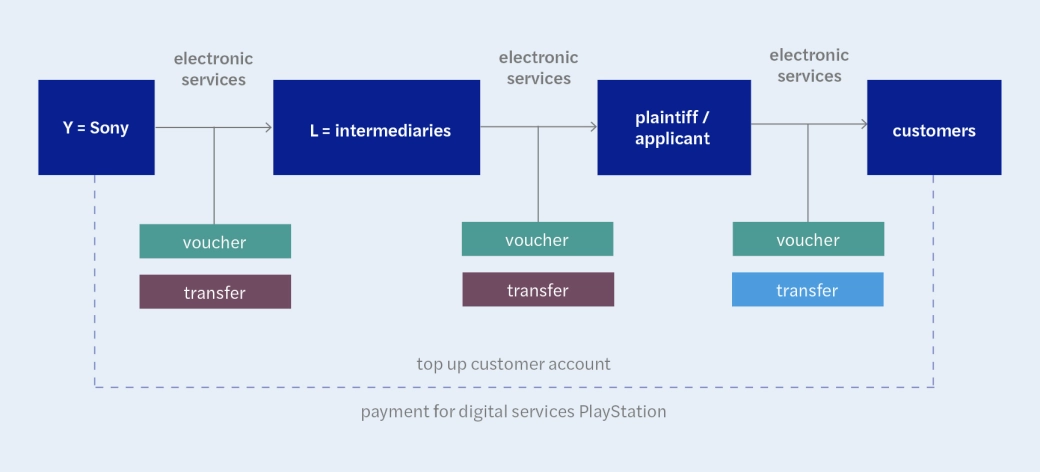

The plaintiff in the regional Financial Court proceedings, who later filed an application for suspension of execution with the BFH for the duration of the appeal proceedings pending there, traded in voucher codes for the purchase of digital content for the PlayStation Network, so-called PSN cards. These PSN cards had been issued by the UK-based company Sony Europe (referred to as "Y" in the BFH ruling). These codes allowed PlayStation users to top up their Sony account and then use that credit to purchase digital services. Sony transferred these voucher codes to intermediaries located in various EU Member States (referred to as "L" in the BFH decision), who then transferred them to the applicant. The applicant later issued the voucher codes to PlayStation users via an online shop.

When customers set up a customer account with Sony, they were asked for their place of residence. German customers were then issued a German customer account. The PSN voucher codes had country codes that identified the country. PSN cards with the country code "DE" could only be redeemed for German customer accounts. The terms and conditions explicitly required the customer to be honest in the use. If Sony became aware that a customer had provided false information, it blocked the customer's account. These measures were intended to ensure that it would be clear when a PSN card with the identifier "DE" was issued that only customers residing in Germany could use the PSN card, thereby ensuring that the place of supply for the digital service pursuant to § 3a (5) sentence 2 no. 3 of the German VAT Code (UStG) was Germany. This would allow the PSN card to be treated as a single-purpose voucher for VAT purposes.

In reality, there were frequent irregularities in this area. Due to price differences between countries, customers sometimes registered in countries other than their country of residence. The plaintiff/applicant therefore argued that when a PSN card with a DE identifier was issued, it was by no means certain that the customer actually resided in Germany. As a result, the place of supply pursuant to § 3a (5) sentence 2 no. 3 UStG is also not certain so that the voucher is not a single-purpose voucher but rather a multi-purpose voucher. The issuance of the PSN Cards by the plaintiff/applicant was therefore not taxable.

Assessment by the Financial Court of Schleswig-Holstein

This argument was already countered by the Schleswig-Holstein Regional Financial Court in the first instance. The place of supply could be sufficiently determined based on the country code system and the terms of use for the normal contractual use of the PSN network. The fact that it is not technically possible to prevent a customer not residing in Germany from using a PSN card with a DE identifier does not prevent the place of supply from being sufficiently determined. In the individual cases in which this can be proven to have actually occurred, a multi-purpose voucher is to be assumed.

The BFH has its doubts

The BFH is bound by the Financial Court's assessment of the facts.

However, the BFH had doubts about the result of the Financial Court for another reason: Neither the UStG nor the VAT Directive explicitly states whether only the place of supply for the supply to the user of the voucher must be determined when the voucher is issued, or additionally the place of supply of the fictitious supplies of the transfers, i.e. the "sales" of the voucher between entrepreneurs before it is sold to a final customer. It is true that in the present case the findings of the Financial Court indicate that it assumes that the PSN cards were only issued to end customers who were private individuals residing in Germany and that the place of supply for the electronic services under § 3a (5) UStG could only be in Germany, the situation is different for the transfer process from Sony Europe to the intermediaries. According to § 3a para. 2 UStG, the place of supply in this transaction is determined by the place where the respective intermediary operates its business - if it is a VAT taxable person at all. Because the intermediaries were located in different EU Member States and it was not yet clear when the PSN cards were issued which intermediary would receive the cards, this place of supply could not yet be determined. The BFH should seriously consider defining a single-purpose voucher as only being one in which the place of transfer is located in the same country as the place of supply of the issue.

Practical implications for the classification

The BFH ruling creates new uncertainties. Entrepreneurs wanting to play it safe here should avoid cross-border chain transactions. If, for example, in the present case it was certain that only German intermediaries were involved, the question raised by the BFH would not have arisen.

In terms of the relationship between the issuer and the end customer, this case also impressively demonstrates the potential conflict inherent in ensuring the place of supply. Although the Financial Court considered the country code system to be sufficient for a single-purpose voucher despite certain technical deficiencies, this decision relates to a specific individual case and should not be generalised. As a matter of principle, a high standard should be aimed at when ensuring the place of residence and, if applicable, also the customer’s potential status as a VAT taxable person.

Contacts

Thomas Pelzer Partner - Berlin