Real Estate

A solid foundation for an uncertain property market

In 2018 the growth of leading European construction companies exceeded 6% for the second year in a row. Following a clear recovery in European and international activity in 2017 (6.9%), growth reached 6.2% in 2018. This is much better than overall European GDP growth (2.4% in 2017 and 1.9% in 2018.) All sectors benefited: building and public works (4.9%), real estate (9.9%), concessions/infrastructure (0.1%), rail and road (11.4%) and energy and services (11.9%).

PANEL GROUP 2018 TURNOVER AND 2018 VS. 2017 GROWTH

Growth was driven by several factors: healthy order, the continuation of large projects, successful international expansion and scaling up via recent acquisitions.

In Europe, transport infrastructure benefited most from the recovery in investment, in particular thanks to major urban projects (Grand Paris Express, Crossrail in London, Greater Dublin Area). The continuation of the European Union’s Juncker Plan should also make it possible to finance €125 billion of public works investments by the end of 2020, adding up to a total of €500 billion since the plan launched in 2015.

Elsewhere in the world, demand is growing for large-scale and increasingly complex projects that require big international operators. In this field, the leading European players know how to take advantage of their size, the variety of their expertise, their drive for innovation and their geographic reach. For example, Balfour Beatty is leveraging its broad international exposure to target countries, such as the UK, the US and Hong Kong, where governments are planning large-scale infrastructure investment for the coming decades.

As a consequence, the contribution of domestic markets to construction companies’ overall revenues continues to decline. In 2018, domestic contributions accounted on average for 45.9% of the groups’ turnovers; but with wide disparities. While domestic contributions made up over 80% for PEAB and 77% for Eiffage, they only added to 14% for ACS and 7% for Salini Impregilo. In many cases, the strength of global revenue streams compounds the risk arising from economic slowdown in the home market – such as Spain, where GDP growth may fall from 3% in 2017 to 1.9% in 2020 – and enhances the resilience of groups with more globally diverse sources of income.

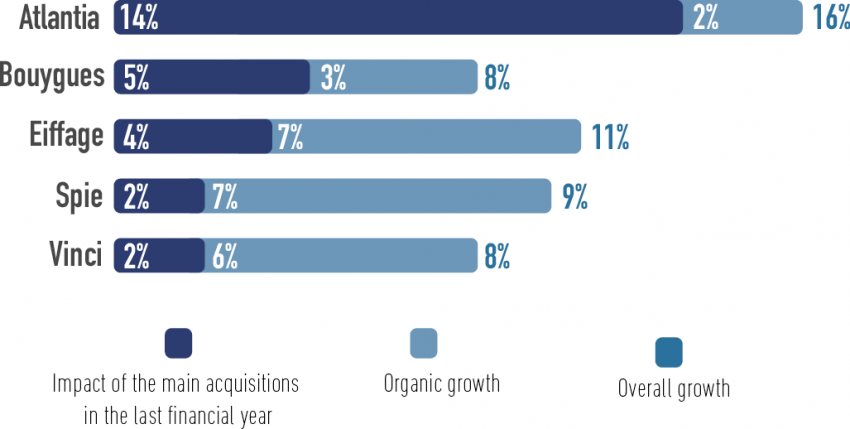

The international footprint of companies covered in our survey expand when large overseas projects are won organically, and via M&A. Several significant acquisitions took place in 2018, enabling these groups to rapidly extend their footprint in dynamic markets and to diversify their business – thereby helping maintain profitability.

IMPACT OF MAIN 2018 ACQUISITIONS ON SAME-YEAR TURNOVER

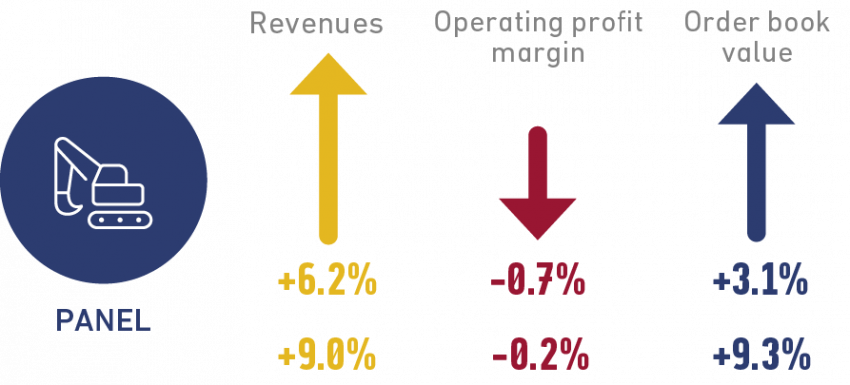

According to the Federation of the European Construction Industry (FIEC), the construction industry should continue to grow, although at a moderate pace (2.2% growth in 2019, versus 1.5% for the overall European GDP forecast). We expect the turnover of large European construction companies to keep increasing in 2019. Our panel’s order books increased by a further 3.1% in 2018, sustaining revenue streams across 2019, albeit activity should growth more moderately than in 2018. In addition, external growth operations carried out in 2018 have been integrated into the first half of 2019, resulting in 10% more business on average than in the first half of 2018.

Turnover growth has not converted into improved profitability yet. After a slight drop of 0.1 point in 2017, operating margin rates fell by 0.7 points to 6.4% in 2018. They declined across all sectors of the panel, but with a wide disparity between groups. Atlantia, NCC AB and Ferrovial, for example, saw their operating margins decline by 10.7, 3.5 and 1.5 points, respectively.

Signals of a market under pressure come from many fronts: the bankruptcy of Carillon in the UK, financial difficulties of some Italian players in a stagnating domestic market and increasingly complex contractual conditions threatening otherwise robust demand across the European market. In addition, subcontracting and raw material costs are rising, and a skilled labour shortage looms. What’s more, the groups’ remain committed to upgrading health and safety standards, social inclusion and diversity, as well as environmental objectives – starting with using more sustainable materials and improving waste management.

To protect margins, the leading European construction players are becoming more selective on projects, balancing their asset and project portfolios, and continuing external growth in a sector that is still not highly concentrated. M&A opportunities may arise in buoyant markets such as Australia and the US, or in fragmented markets such as the UK. In Italy, Salini Impregilo plans to transform itself into a national champion capable of seizing global opportunities by acquiring the number two firm, Astaldi, and other construction companies that are in trouble due to stalled public infrastructure orders.

2018 EVOLUTION OF TURNOVER, OPERATIONAL MARGIN AND ORDER BOOK

European groups highlight initiatives around innovation and areas with strong momentum, among which are airports, environment-friendly construction and smart cities.

With airline traffic up 6% in 2018 and forecast to double by 2037, the airport sector is increasingly attractive to leading European construction players, with several of them – Atlantia, Balfour Beatty, Eiffage, FCC and Vinci – developing this business line through M&A. Vinci Airports alone recently secured concessions for Salvador Airport in Brazil, Kobe Airport in Japan and Belgrade Airport in Serbia; acquired Airport Worldwide, which operates eight airports; and signed an agreement to become the majority shareholder of London Gatwick Airport. All four groups and other leading players are expected to keep targeting international markets, especially in North America and Europe. In France, all eyes are on the potential privatisation of Aéroports de Paris (ADP group).

Some companies in our panel are working to meet the Paris agreement to reach carbon neutrality by 2050, and to comply with the low-carbon regulations of the future European Energy Law. Actively seeking ways to reduce their environment footprint, many are investing in the wood sector, where they see strong potential. They intend to develop their know-how by focusing on three-dimensional modular construction, as well as the construction of high-rise buildings with wooden structures.

Smart cities will also provide effective responses to climate challenges by rethinking how residents and the administration interact and by leveraging social and technological innovations to develop the economy, facilitate mobility and care for the environment – from energy to water and waste management issues. Alongside iconic projects such as New Songdo City, smaller towns are also embracing the trend. In 2018, 25 French cities began developing intelligent services for smarter, greener urban lives. The creation and evolution of these new urban areas offer a wealth of opportunities to forward-looking construction players.

Sources and methodology

Mazars’ annual study of listed European construction companies includes pure players or diversified groups with a consolidated turnover of €5 billion and above. It analyses annual reports and reference documents from the 17 companies that are part of this year’s panel, sector information published by the Federation of the European Construction Industry (FIEC), as well as Xerfi and Bloomberg data. Read the full report (in French).

A solid foundation for an uncertain property market

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.