Effective income tax (ISR) rate for large taxpayers

InsightsForvis Mazars in Mexico: Thought leadershipTax alert

Effective income tax rate for large taxpayers

According to the current framework of the powers granted to the Tax Administration Service (SAT) by the 2021 Tax Reform, and with the aim of facilitating and encouraging voluntary compliance by taxpayers, last June 13, 2021, the SAT, on its portal, published the first parameters regarding the effective Income Tax rates, corresponding to 40 economic activities with regards to the 2016, 2017, 2018 and 2019 tax years, corresponding to the list of major taxpayers.

It’s worth pointing out that the economic sectors covered by these first 40 economic activities include the following:

- Mining

- Manufacturing

- Wholesale commerce

- Retail commerce

- Financial services

- Insurance

Along these lines and with the aim of facilitating and encouraging voluntary compliance, the SAT makes a cordial invitation to taxpayers to consult the effective tax rate corresponding to the economic activity to which they belong and make a comparison with the effective rate actually calculated regarding each tax year so as to measure their tax risks and, if applicable, make the pertinent corrections by means of the filing of complementary tax returns corresponding to the tax year and consequently minimize the possibility of the start of in-depth revisions aimed at corroborating the correct fulfillment of the tax obligations of taxpayers.

It is important to point out that, for the purposes of this analysis to be performed by taxpayers, they should take into account the following definitions:

Tax risk

Contingency of noncompliance with fiscal provisions that are applicable to a taxpayer or group of taxpayers and which affects the correct payment of taxes, specifically on matters of income tax.

Economic activities

Those contained in Annex 6 of the Miscellaneous Tax Resolution in force and which each taxpayer has selected in its fiscal information filed with the SAT.

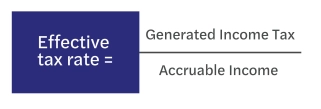

Effective tax rate

That calculated using the information stated in the last annual Income Tax return corresponding to the tax year, in accordance with the following:

As can be seen, the corresponding analyses will have to be carried out in order to foresee any difference and, if one exists, assess the impact that this would have so as to be able to make the respective corrections, and to this end. At Mazars we are at your full disposal to help you with any doubts or concerns you may have.

Want to know more?