SOC 1

Report on controls around the user's financial information in a service organization. Our clients must have confidence in any processes that affect financial statements. This report seeks to demonstrate the productivity and effectiveness of internal financial reporting controls.

SOC 2

Reporting controls around security, availability, processing integrity, confidentiality, or privacy in a service organization. Feeling confident about the information control environment is an invaluable asset that you can offer to your customers.

SOC 3

Report that provides customers with reliability on the SOC 2 report. Normally, SOC 3 reports can be freely shared and published on the internet. This report shows a little of the auditor's opinion, as well as language that provides context about the organization and the relevant IT infrastructure. This does not mean that no audit testing is required, but that it is done to provide certainty about the control environments described in SOC 2. This report does not contain much detail about the controls, which is why it can be shared without concerns.

Which SOC report does my organization need?

What to do to be prepared?

- Determine the type of report and the standard to be applied.

- Review the current description of the systems and controls to be validated, if appropriate. If necessary, strengthen internal control and risk management.

- Review the standards to gain additional knowledge about the requirements.

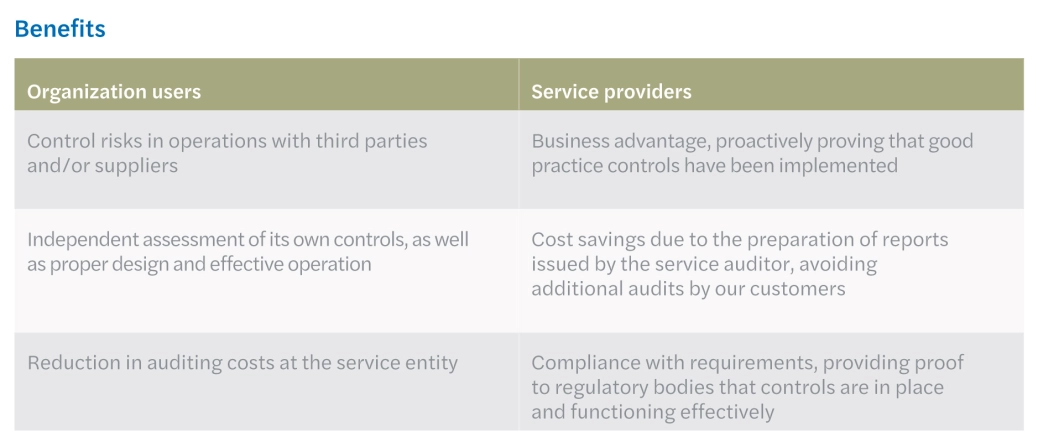

Benefits

Want to know more?

Rodrigo Enrique Romero Rodríguez Consulting Lead Partner - Ciudad de México (Mexico City)