IFRS S1 and S2: new sustainability and climate standards for businesses

InsightsForvis Mazars in Mexico: Thought leadershipFinancial alert

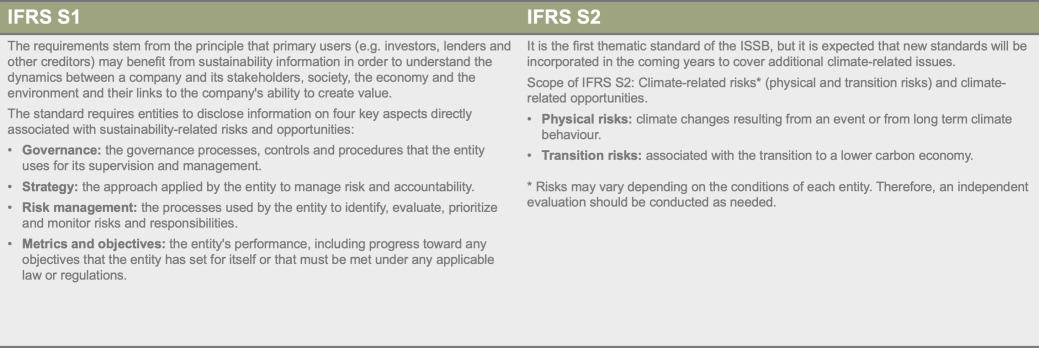

IFRS S1 and S2: sustainability and climate

On June 26, 2023, the International Sustainability Standards Board (ISSB) published the first two IFRS Sustainability-Related Disclosure Standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-Related Disclosures).

Both standards issued by the ISSB lay the foundation for a global framework of sustainability-related disclosures and derive their foundation from a number of globally accepted standards and reports, most notably the Task Force on Climate-related Financial Disclosures (TCFD) and the Sustainability Accounting Standards Board (SASB). Likewise, its compatibility with European sustainability standards will be key for companies to avoid redundant reporting. In turn, the ISSB is also committed to working with the Global Reporting Initiative (GRI) to ensure that its standards are complementary and compatible with those of the GRI.

The standards issued by the ISSB have been designed to complement the International Financial Reporting Standards (IFRS), used by over 140 jurisdictions worldwide and, although the ISSB does not have the right to mandate their application, companies can apply them voluntarily and local authorities can decide whether companies should apply them. Some jurisdictions have already announced their intention to adopt the standards, especially in emerging and developing markets, including Mexico.

To learn more about the new ISSB standards, their history, the benefits of their application, as well as the main challenges, solutions and key points that need to be considered for a successful implementation, download our publication "IFRS S1 and S2: new sustainability and climate standards for businesses".

Want to know more?