Corporate income tax alert

1. Reform of Belgian Investment Deduction

The Belgian Investment Deduction reform aims to:

- Modernize the list of investments eligible for this regime after 40 years.

- Align with sustainable development needs.

- Establish fixed percentages and simplify procedures.

The new system is set to commence as from 1 January 2025, but is still subject to legislative approval.

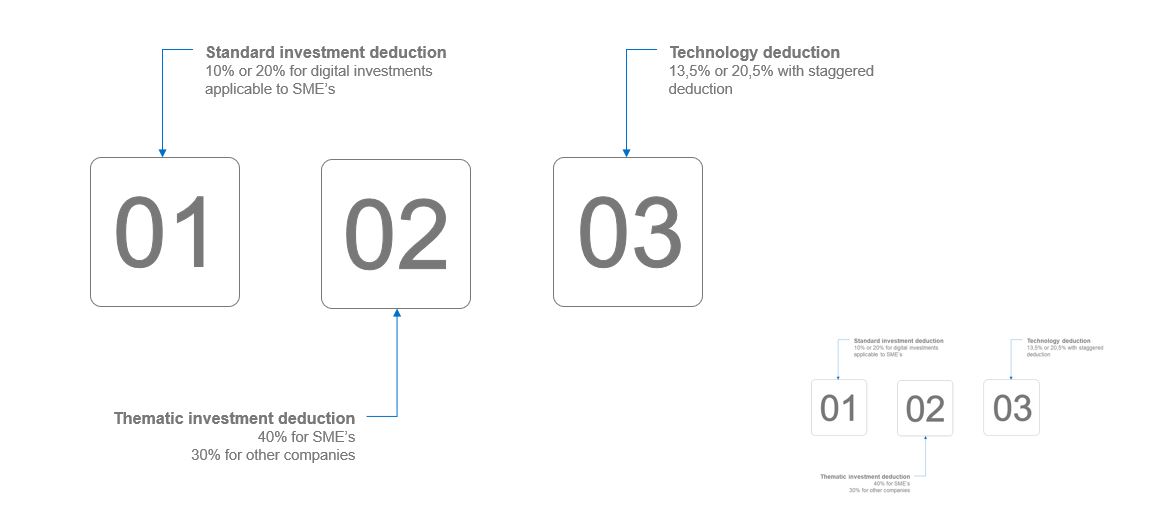

The new system comprises three tracks:

The table below provides an overview of the current system of qualifying investments and the percentages for the fiscal years 2022, 2023, and 2024.

| Small and medium-sized companies (SME’s) (1) | 2022 | 2023 | 2024 (2) |

| Ordinary investment deduction - one-off | 25% | 8% | 8% |

| Digital investments - one-off | 13,50% | 20,50% | 15,50% |

| Security - one-time | 20,50% | 27,50% | 22,50% |

(1) also applicable to self-employed individuals

(2) expected percentage for fiscal year 2024 (tax year 2025). To be confirmed via publication in the Belgian Gazette.

| All companies | 2022 | 2023 | 2024 (2) |

| Environmentally-friendly investments in R&D - one-off | 13,50% | 20,50% | 15,50% |

| Environmentally-friendly investments in R&D - staggered | 20,50% | 27,50% | 22,50% |

| Patents - one-off | 13,50% | 20,50% | 15,50% |

| Energy-saving investments - one-off | 13,50% | 20,50% | 15,50% |

| Fume extraction or ventilation systems - one-off | 13,50% | 20,50% | 15,50% |

| Greening of trucks and refuelling infrastructure - one-off | 35% | 42% / 36,50% | 31,50% |

| Reusable packaging - one-time | 3% | 3% | 3% |

| Companies exclusively active in maritime shipping | 2022 | 2023 | 2024 |

| Sea-going vessels - one-off | 30% | 30% | 30% |

The table below provides an overview of the “tracks” and the percentages that would apply as from 2025.

| New investment deduction from 01/01/2025 | SME's (3) | Other companies |

| General track: basic deduction - one-time | 10% | - |

| General track: digital investments - one-time | 20% | - |

| Thematic deductions - one-time | 40% | 30% |

| Technology deduction for R&D and patents - one-time | 13,50% | 13,50% |

| Technology deduction for R&D - spread out | 20,50% | 20,50% |

| Ships - one-time | 30% | 30% |

(3) also applicable to self-employed individuals

1) General track for small and medium-sized companies (SME’s):

- Basic deduction increased from 8% to 10% exclusively for SMEs

- Simplified application process without formal requirements

- Excludes assets with harmful environmental impact unless no alternative is available

- Additional 10% deduction for digital investments by small and medium-sized companies

- The eligible investments include software and equipment supporting digital payment and invoicing systems, digital accounting systems, digital CRM systems, digital e-commerce platform systems, and digital systems for securing information and communication technology. The specific nature and technical features of the qualifying investments will be defined by royal decree.

- Annex 275U should be added to the corporate income tax return

2) Targeted track: thematic deductions:

- Offers higher deductions for specific investments and technologies

- Applicable to all companies with a 40% deduction for small and medium-sized companies and 30% for others

- Categories include energy efficiency, renewable energy, zero-emission transportation, and digital investments aligned with these themes

3) Transformation of research and development investment allowance:

- Introduction of Technology Deduction offering a 13,50% deduction for qualifying R&D investments and patents

- Increased to 20,50% if deduction is spread over time, excluding investments in patents

- Option for taxpayers to opt for a tax credit

Implementation:

- Expected as from 1 January 2025

- Details to be determined by Royal Decree, influencing Belgium’s investment landscape

Example : Investment in zero-emission truck ad 60.000 EUR, depreciated over 10 years

| Thematic investment deduction (one-off) | Company A | Company B |

| Revenue | 150.000 | 150.000 |

| Depreciation zero-emission truck | -6.000 | 0 |

| Taxable profit | 144.000 | 150.000 |

| Investment deduction (30%) | -18.000 | 0 |

| Taxable base | 126.000 | 150.000 |

| Corporate income tax | 31.500 | 37.500 |

Consider the following scenario: Company A and Company B, both large companies, generate both a revenue of 150 KEUR during the year 2025. However, Company A makes a strategic decision to invest 60 KEUR in a zero-emission truck, whereas Company B does not pursue the same investment opportunity.

Company A benefits from a thematic (one-time) investment deduction of 30% due to its investment in the zero-emissions truck. As a result, Company A’s taxable base decreases to 126 KEUR after deducting the 18 KEUR investment deduction. As a result Company A would be liable to a corporate income tax of 31,5 KEUR.

On the other hand, Company B chooses not to utilize the investment deduction. Therefore, its entire profit becomes taxable. Assuming that no additional costs are present, this would result in a corporate income tax liability of 37,5 KEUR.

The decision to invest in a zero-emission truck at 60 KEUR results in a decreased taxable basis for Company A, attributed to the additional annual depreciation of 6 KEUR and the one-time investment deduction of 18 KEUR. Consequently, leading to a net tax saving of 6 KEUR for Company A.

2. 120% deductibility for E-invoicing costs

- Costs for e-invoicing are 120% deductible for small and medium-sized companies starting from 1 January 2024.

- The law of 6 February 2024, obliges electronic invoicing between VAT-registered businesses from 1 January 2026.

- Eligible investments for the enhanced 120% deduction include billing software enabling structured electronic invoicing, periodic subscription fees for such software and consultancy costs related to compliance with these obligations.

- It only concerns direct costs related to preparing for compliance with electronic invoicing obligations

- Costs that are capitalized and depreciated are not eligible for the enhanced deduction.

Want to know more?