Covid-19: Operating lease rent concessions given by lessors

Who we areNews and publicationsOur publicationsForvis Mazars MessengerMazars Messenger November 2020

Operating lease rent concessions given by lessors

The ongoing COVID-19 pandemic has significantly reshaped the world we live in and how we account for certain transactions. One such affected transaction includes how lessees and lessors account for their leases under IFRS 16 Leases (‘IFRS 16’).

The pandemic has caused much financial hardship on lessees in making their lease payments, and as a result, lessors have looked to providing specific COVID-19 rent concessions to ease the economic impact of the pandemic.

The International Accounting Standards Board (‘IASB’) has amended IFRS 16 relating to how lessees account for rent concessions as a result of COVID-19. These amendments provide lessees with a practical expedient that allows a lessee an accounting policy choice for rent concessions. The lessee may choose to account for these as either a once-off reduction in rent by accounting for it as a variable lease expense through profit or loss or as a lease modification. These amendments are applicable immediately due to the ongoing pandemic.

It is important to note, however, that these amendments are not applicable to lessors who provide their lessees with COVID-19 rent concessions.

So what does IFRS 16 say about how a lessor should account for COVID-19 rent concessions?

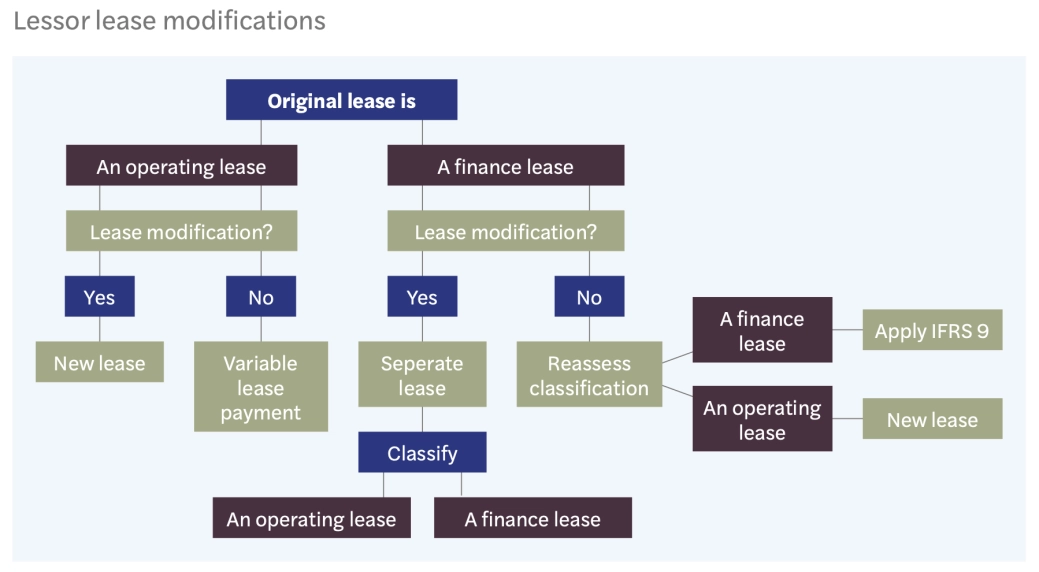

Lessors must continue to account for COVID-19 rent concessions by applying the specific lease modification guidance in IFRS 16 (i.e. paragraphs 79-80 and 87). The lessor must determine if the rent concession meets the definition of a lease modification. The definition of a lease modification applies equally to lessees and lessors, except that for lessors, rent concessions accounting treatment will depend on the classification of the lease.

What is a lease modification?

Changes to the scope of a lease or to the lease term and/or lease consideration of the original contract terms are lease modifications. Examples of lease modifications can include increasing or decreasing the scope of a lease (i.e. adding or removing the right to use one or more underlying assets, shortening or increasing the contractual term or by increasing or decreasing lease payments.)

The diagram below summarises the accounting treatment relating to a rent concession for an operating lease or finance lease: accrued lease payments relating to the original lease as part of the lease payment for the new lease). The lessor recognises lease income on a systematic basis that represents the pattern in which the underlying asset is used.

Where a lessor modifies a finance lease, the lessor will need to reassess the lease classification. A modification that increases the scope and consideration of the lease by an amount that is commensurate with the stand-alone price is accounted for as a separate lease.

For finance leases that are modified that do not result in a separate lease, the lessor will assess whether the classification of the lease would have been different if the modified terms had been effective at inception date. If the lessor determines the modified lease would have been classified as an operating lease at inception date, then the lessor accounts for the lease as a new lease from the effective date of the modification.

If the modified lease would have remained a finance lease at the inception of the lease, the lessor then applies IFRS 9 Financial Instruments (‘IFRS 9’) and adjusts its measurement of the lease receivable to reflect any reduction in future contractual lease payments that arise from giving its lessee a COVID-19 rent concession, recognising a modification gain or loss.

What does a lessor do if the concessions on an operating lease do not meet the definition of a lease modification?

If a change that is part of the original terms of the lease does not meet the definition of a lease modification, the lessor will generally account for such a change as a variable lease payment, i.e. the lessor recognises a reduced operating lease income during the concession period only.

What are significant changes to lease payments that would lead to a lease modification?

Lease deferrals deferred by a lessor for a period of time (say three months) that are recovered from the lessee at a later stage, are essentially ‘catch- up’ or deferred lease payments. In such cases, the lease consideration is unchanged as such a lease payment deferral has not changed the scope or the consideration significantly, such a deferral just affords the lessee cash flow relief. Such deferrals are not considered to be lease modifications.

Further to this, if the lessor includes the time value of money in a subsequent period to recover the deferred lease payments, such time value of money is not considered to be significant enough to warrant a change in lease consideration and would not be considered a lease modification as opposed to a more significant change in lease payments like forgiveness of lease payments would be considered a lease modification.

How does a lessor assess the definition of a lease modification?

The lessor will assess whether the rent concession meets the definition of a lease modification as discussed above. The below are some examples relating to COVID-19 operating lease rent concession scenarios that could be seen in practice:

What does South African Law and IFRS 16 have to do with one another?

The COVID-19 pandemic around the world has also brought about some legislative changes. Governments and certain jurisdictions have introduced laws that require lessors to provide lessees with certain rent concessions to assist with the economic impact of the pandemic. As a result of such legislation, the applicability of the definition of a lease modification needs to be more closely considered and assessed.

In South Africa, in the absence of a force majeure clause in a lease agreement, common law takes precedence. Under South African common law, a lessee may be entitled to request a rent concession (or ‘remission of rent’) due to loss of use of the leased asset as a result of unforeseen circumstances not in the control of the lessee.

This was quite true during the beginning of our hard lockdown where many businesses were forced to cease trading and shut down for a period of time. IFRS 16, unfortunately, does not provide guidance around such legal modifications, so, therefore, there will be diversity in practice in considering whether a legal requirement to provide a rent concession is a lease modification or not. Preparers could either interpret a legal requirement to provide a rent concession as a change to the original terms of a lease agreement or that such legal requirement bounds the lessee and lessor to the agreement in the jurisdiction the lease agreement was entered into and any changes in legislation would not be considered a lease modification.

What else should lessors consider when providing operating lease COVID-19 rent concessions?

Lessors should assess whether the underlying asset, operating lease income and related lease receivables are measured appropriately.

IAS 36 Impairment of Assets should be applied to property, plant and equipment, a right-of-use asset that is not investment property and investment property measured at cost. For investment property measured at fair value, the lessor must ensure that the fair value of the investment property reflects the fair value in an active market. The lessor must consider whether operating lease income and their lease receivable is correctly recognised and in line with the enforceable terms of the lease, which involves assessment of whether the rent concession meets the definition of a lease modification.

The lessor must apply IFRS 9 to operating lease receivables and monitor their recoverability in terms of this standard accordingly. IFRS 16 does not require any specific disclosure in respect of lease modifications as a result of COVID-19 rent concessions. It is, however, advisable for the lessor disclose information (i.e. information that impacts the financial position, financial performance and cash flows) that will assist users of the lessors financial statements to assess and understand the effect of the COVID-19 rent concessions.

Final thoughts

The COVID-19 pandemic is proving to be a trying time for IFRS preparers. There is a lot to consider

in a many areas of IFRS with one of them on leases. Lease modifications in terms of IFRS 16 are not easy and can become complex to apply. Judgement will also need to be applied in determining whether a rent concession meets the definition of a lease modification or not. Lessors will have to relook at the terms of the lease and the agreed terms of the rent concession with the lessee and consider all the facts and circumstances for each lease before determining the accounting impact.

Our experts