Revenue recognition: Disaggregation disclosure decisions

27 November 2024

Revenue generation is core to most entities. Disclosure of revenue is therefore vital to understanding the business. The disaggregation thereof gives additional insight to support decision making.

According to paragraph 114 of IFRS 15 Revenue from Contracts with Customers (IFRS 15), “an entity shall disaggregate revenue recognised from contracts with customers into categories that depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.”

Why it is important to disaggregate revenue? What must be considered when disaggregating? Where else is disaggregation information provided? Is there a link between the IFRS 15 disaggregation requirements and other Standards? All these questions will be answered as we delve into the disaggregation complexities.

Why is it important to disaggregate revenue?

Revenue has traditionally been presented as a single line item in the financial statements, not giving much insight as to what it consists of, which is particularly relevant to entities who sell a mix of goods and/or services. Entities also have different customers, for example, governments, blue chip companies and/or even small owner-managed businesses, and sell to different geographical regions, in different provinces within a country, or different countries. The different customers or customer portfolios expose the entity to different risks through the types of products or services provided, different payment profiles and even different trends and cycles. The geographical regions also bear different risks, especially with regards to red-tape and trying to get the cash from outside of the country is influenced by very different macro and micro economic factors. It is important that the composition of revenue be available to users of financial statements to allow them to make their decisions with an understanding of the key revenue influencers.

The JSE has repeatedly noted instances of insufficient disaggregation; it was a focus area.

In the combined findings report1 issued 28 October 2022, the JSE states, “We continued to find instances of insufficient disaggregation of revenue.” Further, in the same report, the JSE reported that there were issuers who “did not disaggregate their revenue into sufficient categories.”

Dealing with disaggregation is important for analysis and decision-making, as well as a regulatory issue.

What must be considered when disaggregating?

Per IFRS 15.114, revenue must be disaggregated “into categories that depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.”

The starting point in dealing with disaggregation is the type of categories to use. Per IFRS 15.B88, “an entity shall consider how information about the entity’s revenue has been presented for other purposes, including all of the following: (a) disclosures presented outside the financial statements (for example, in earnings releases, annual reports or investor presentation); (b) information regularly reviewed by the chief operating decision-maker for evaluating the performance of operating segments; and (c) other information that is similar to the types of information identified in paragraphs B88(a) and (b) that is used by the entity or users of the entity’s financial statements to evaluate the entity’s financial performance or make resource allocation decisions.”

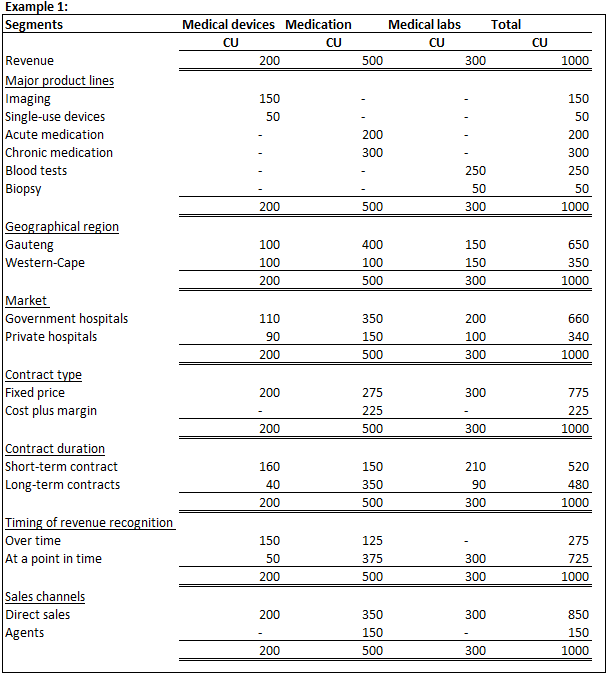

To illustrate the above points, let us consider the example of Health Co below.

Health Co (Pty) Ltd “Health Co” is a supplier of medical equipment and consumables2. Health Co’s revenue information has been extracted from the management accounts and summarised below. Health Co reports the following operating segments: medical devices, medication, and medical laboratories, and uses Currency Units “CU” as its functional and presentation currency.

The following facts are relevant to the Health Co example:

- Health Co presents information about major product lines, markets, and timing of revenue recognition in its annual report and investor presentations.

- The chief operating decision maker evaluates performance based on major product lines and geographical regions.

In determining the categories to use for revenue disaggregation preparers of the Health Co financial statements should consider major product lines, markets, timing of revenue recognition, and geographical region as the categories that depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

Although information about contract type, contract duration and sales channels is available, it is important that revenue is disaggregated into categories that are meaningful to the business of Health Co, and the users of the financial statements. The provision of information that is too detailed or not meaningful to the business may result in cluttered disclosures.

On the other hand, by way of example, Medi Quip (Pty) Ltd3 “Medi Quip”, operating in the same industry as Health Co, only presents information about major product lines and geographical region in its annual report, and evaluates performance and resource allocation based on the major product lines. The categories that Medi Quip considers in disaggregating revenue are the major product lines and geographical regions. However, if both Health Co and Medi Quip operate in an industry with regulated sales to government hospitals, for example, then Medi Quip should also consider markets as a category to disaggregate revenue.

The Medi Quip example not only highlights the fact that both industry and entity specific factors need to be considered in disaggregating revenue, but also that, “some entities may need to use more than one type of category to meet the objective in paragraph 114 for disaggregating revenue (IFRS 15.B87).”

When assessing the revenue disaggregation disclosures provided, a useful completeness check can be performed by reviewing the requirements of IFRS 15.B89. In terms of the paragraph, “examples of categories that might be appropriate include, but are not limited to, all of the following:

a) type of good or service (for example, major product lines);

b) geographical region (for example, country or region);

c) market or type of customer (for example, government and non-government customers);

d) type of contract (for example, fixed-price and time-and-materials contracts);

e) contract duration (for example, short-term and long-term contracts);

f) timing of transfer of goods or services (for example, revenue from goods or services transferred to customers at a point in time and revenue from goods or services transferred over time); and

g) sales channels (for example, goods sold directly to consumers and goods sold through intermediaries).”

This list is a suggestion, i.e., there is no requirement to provide all seven disaggregation categories. Furthermore, the seven categories listed are not exhaustive, i.e., there may be other categories that could provide useful information. One such category that can be considered, if relevant, is the in-store versus online sales which is particularly relevant in our changing consumer environment. Nevertheless, the list provides a good starting point when scrutinising revenue disaggregation disclosures.

Where else is disaggregation information provided?

When regulators review financial statements, they do not limit their review to the information provided within the financial statements. Entities often provide a detailed analysis, both narrative and numerical, when describing the entity’s performance during the year. This can be reflected in an entity’s annual report, integrated report, directors’ report or management discussion and analysis. It is expected that if an analysis is provided elsewhere, this level of information is probably important enough to be disclosed within the financial statements.

Is there a link between the IFRS 15 disaggregation requirements and other Standards?

The most obvious link between disaggregation in terms of IFRS 15 and other Standards is IFRS 8 Operating Segments. Paragraph 115 of IFRS 15 states, “In addition, an entity shall disclose sufficient information to enable users of financial statements to understand the relationship between the disclosure of disaggregated revenue… and revenue information that is disclosed for each reportable segment…”

In the Health Co example, the company reported revenue for three segments. Health Co then disclosed disaggregated revenue in a manner that demonstrates how revenue for each segment reconciles to the disaggregated revenue per segment and in total. This achieves the requirement in IFRS 15.115. It is important, however, to note that presentation in terms of IFRS 8 does not always achieve the objective of IFRS 15.114. As the JSE stated in the 2022 proactive monitoring report, “whilst segmental information is a useful starting point, it is not the end point.”

IFRS 15 disaggregation is also required to be applied in financial reports prepared in accordance with IAS 34 Interim Financial Reporting. In the 2022 proactive monitoring report, the JSE has noted “a lack of disaggregation of revenue on the same level as is presented in the AFS.” This requirement, from IAS 34.16A(l), must not be overlooked.

Final thoughts

The process applied to determine revenue disaggregation categories need not be complex. It is important to understand what influences the cash flows and risks of sales. It can get more difficult when entity and industry specific facts and circumstances change from year end to year end, and even from year end to interim reporting period. The above examples indicate that there is no one-size-fits-all solution when determining the revenue disaggregation categories. Preparers of financial statements and auditors should not only stay up to date with the revenue mechanisms of entities, but also understand what other disclosures are made outside the annual financial statements, what is important to the business, and how decisions about performance and resource allocations are made.

1 Worded in their report: “We continued to find instances of insufficient disaggregation of revenue.” Combined findings of the JSE proactive monitoring of financial statements: Issued 28 October 2022.

2 Health Co (Pty) Ltd is a fictional company that has been specifically designed for the purpose of serving as an illustrative example within the article.

3 Medi Quip (Pty) Ltd is also a fictitious company that has been specifically designed for the purpose of serving as an illustrative example within the article.

Want to know more?