Dealing with FX: Understanding Foreign Exchange and Its Accounting Impacts

Foreign Exchange (FX) has become a critical component of financial reporting for modern businesses. As companies increasingly engage in cross-border transactions, it is their responsibility to carefully account for the impact of fluctuating exchange rates on their financial statements. Whether they’re working with foreign suppliers, generating revenue from international customers, or managing subsidiaries abroad, accounting for FX accurately is now an essential part of global business operations.

Key Concepts: FX Translation

There are two primary situations in which FX translation plays a crucial role:

- Transactional Currency to Functional Currency – Conversion of foreign currency transactions. For example, when a company sells a product in USD however the business operates primarily in GBP, said entity must translate each transaction into GBP for accurate reporting at the individual reporting level.

- Functional Currency to Reporting Currency – Conversely, when a company has foreign subsidiaries, the financial statements at a subsidiary level are typically prepared using the local functional currency of that entity. When the group is eventually consolidated, a translation from local functional currency to group reporting currency needs to occur. For instance, an Israeli subsidiary might report in NIS at a local level, however their parent company may report in USD. The subsidiary’s financial data must be translated to USD for group reporting purposes.

Types of FX Transactions

- Income and Expenses - All income and expense transactions occurring in a foreign currency must be translated into the relevant functional currency at the spot rate on the transaction date when the transaction occurs. Some companies opt to use an average exchange rate for simplicity as long as the rate remains observable and reliable.

- Non-monetary Assets - Non-monetary assets such as fixed assets, intangible assets, and investments are translated at the exchange rate on the date of the transaction and are not revalued afterward. I.e. the recording of non-monetary assets is done at the historical rate of purchase.

- Monetary Assets - Monetary assets, such as foreign bank accounts, creditors, or debtors, are translated at the period-end spot rate to reflect their current fair value in the functional currency.

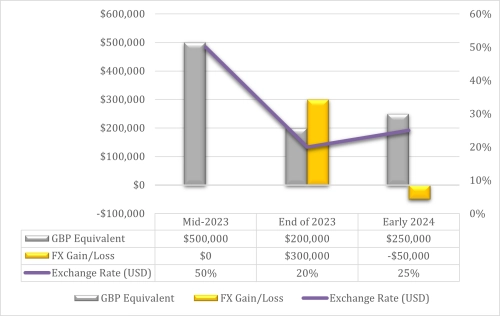

Practical Example: FX Impact on Assets and Liabilities

Let’s consider an example with simplified details, where a company’s functional currency is GBP, and the company purchases a machine from a US supplier for $1,000,000. The asset was recognised in the books in Mid-2023 and the outstanding debt was paid to the supplier in early 2024:

- Mid-2023 – The exchange rate is USD 2: GBP 1 on the date of purchase; as such, the machine is initially recorded at £500,000, with a corresponding liability of the same amount.

- End of 2023 – The exchange rate shifts to USD 5: GBP 1, reducing the liability to £200,000. The company gains £300,000 due to this shift, which is recorded as a foreign exchange gain.

- Early 2024 – The exchange rate adjusts again to USD 4: GBP 1 (a volatile period indeed), and the company ultimately settles the debt for £250,000. However, since the liability was revalued to £200,000 at year-end, an FX loss of £50,000 is now recorded.

- The value of the machine at £500,000 does not change after initial recognition.

A Glance at FX in Group Companies

When dealing with group companies that own multiple foreign subsidiaries, the process of FX translation becomes increasingly complex. The financial statements of each subsidiary must be translated into the group’s reporting currency, which involves additional layers of translation and consolidation. Below are some practical tips to assist in the consolidation process:

To manage FX effectively, here are some practical tips:

- Use Reliable Exchange Rates – Always source exchange rates from a trustworthy provider and verify that your data and formulas are accurate. This avoids costly errors.

- Focus on the Bigger Picture – While technical details matter, don’t lose sight of the overall goal: accurately presenting the company’s financial position.

- Understand Client Processes – If you work with clients, align with their FX translation process before starting. This minimizes confusion and smoothens the process.

- Maintain Clear Audit Trails – Document every conversion, especially with multiple foreign entities. A detailed audit trail ensures transparency and simplifies audits later.

- Have a thorough review process – Ensure more than one person signs off on this consolidation; this will allow for better identification of errors and correction thereof.

In summary, a well-considered approach can assist in managing the complexity of FX transactions. It is vital to ensure accurate and transparent financial reporting across global operations. As entities continue to expand worldwide, the application of FX reporting and auditing thereof will continue to increase in importance. Consistent and repeatable applications across territories and geographies will be the driving forces behind successful FX processing.

Want to know more?