How to understand the key issues of IFRS 15?

ServicesAudit & assuranceCorporate reportingWhat challenges are you facing?International Financial Reporting Standards (IFRS)

How to understand the key issues of IFRS 15?

To both help understand the key issues of IFRS 15 Revenue from contracts with customers (“IFRS 15”) and provide answers to your specific questions, Forvis Mazars publishes "IFRS 15: Key points of the revenue recognition standard in 100 Questions & Answers". This publication, from the Forvis Mazars Insight series, presents the intricacies of a complex standard in a pedagogical way. There is no significant difference between IFRS 15 and Singapore Financial Reporting Standard (International) (“SFRS(I)”) 15 Revenue from contracts with customers or Singapore Financial Reporting Standards (“SFRS”) 115 Revenue from contracts with customers.

Implementation of IFRS 15 since January 1st 2018 may be complex, as it requires an entity to:

- Understand the intricacies of numerous different concepts (control, performance obligations, stand-alone selling price, costs incurred to fulfil a contract, etc.)

- Comply with the principles set out in each step of the revenue recognition model, and

- Make frequent use of judgement while taking account of the facts and circumstances of each specific situation.

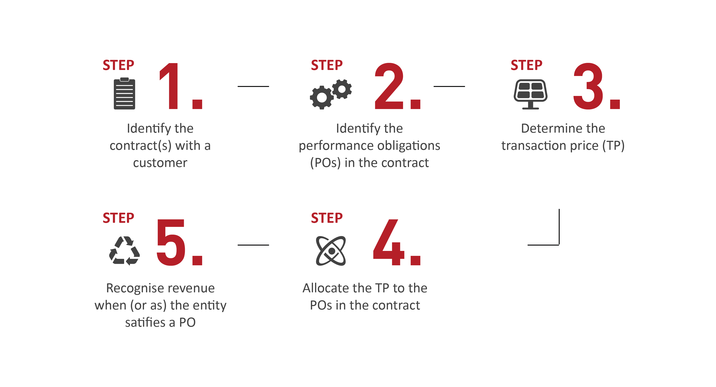

IFRS 15 - Five-step revenue recognition model

In addition to the revenue recognition issues (IFRS 15 introduces a single five-step revenue recognition model that is applicable to all types of contracts with customers in all sectors), entities must also pay close attention to the disclosures in the notes to the financial statements, in order to ensure that they comply with the requirements of the Standard. This is one of the main areas of focus for the regulators in their reviews of the first annual financial statements of 2018 published in compliance with IFRS 15.

This guide in 100 questions and answers is meant to serve as a useful tool for as many stakeholders as possible, providing clarity and insight on the challenging issues at stake when implementing IFRS 15. It does not aim to cover every possible situation that may be encountered in practice, but many topics are examined in detail.

To find out our guide about IFRS 15 - Revenue recognition standards in 100 questions & answers. Download below:

Contact